You have always wanted to Bypass OTP And Withdraw Money From Bank Account? Well, congratulations 🎉

Welcome onboard, on this article you are going to learn 3 Steps To Bypass OTP And Withdraw Money From Bank Account in three (3) easy steps.

Bypass OTP And Withdraw Money From Bank Account

Before we dive into the 3 steps to Bypass OTP And Withdraw Money From Bank Account, you must have the following available or confirmed, contact us if you need help and for more info.

You must have the information of the bank account you are targeting.

You must confirm a debit/credit card is linked to the bank account.

You must have an offshore bank account or a DEX crypto wallet address you are ready to move the funds to.

What Is DEX Crypto Wallet?

Dex means, a decentralized exchange (DEX), decentralized platforms are non-custodial, meaning a user remains in control of their private keys when transacting on a DEX platform.

Why Should I Use Dex Crypto Wallet?

Lack of Oversight: DEXs operate with limited user oversight. There’s no central administrator monitoring accounts, records, identities, or transactions, making it easier for criminals to hide their activities. Crypto-to-Crypto Swaps: DEXs facilitate seamless swaps between different cryptocurrencies.

3 Steps To Bypass OTP And Withdraw Money From Bank Account

STEP ONE: Get the bank card details

Card number

Card expiry date

CVV number

Card name

billing address (optional)

When you have all the above information complete, move on to the step two.

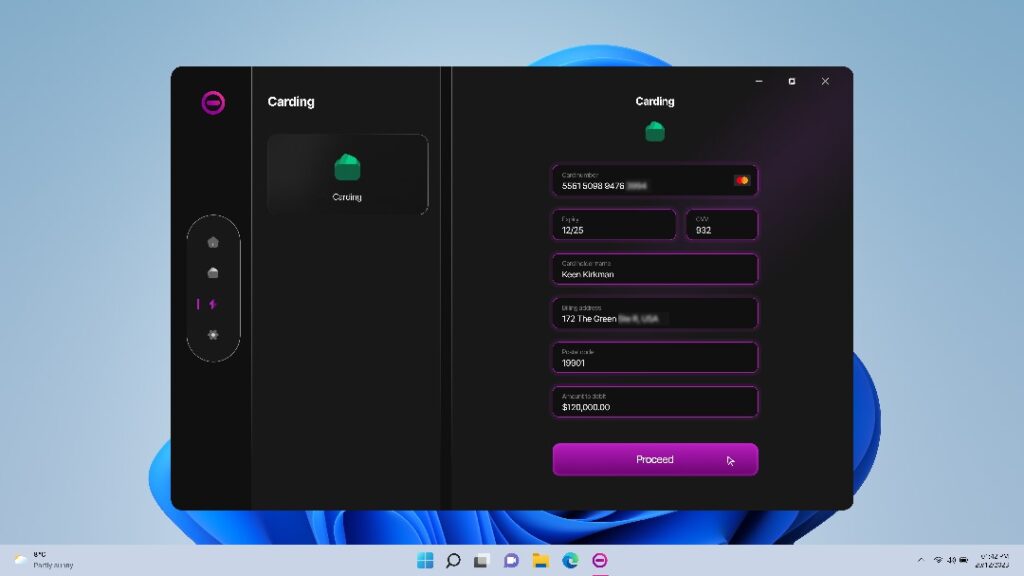

STEP TWO: Get a carding software

What Is A Carding Software?

A carding software is a software or technology widely used by hackers and cyber criminals to withdraw money from bank cards without authorisation, kindly refer to the following screenshot of the carding software.

How Can I Get Carding Software?

To get a carding software for advanced carding transaction is not difficult, simply contact our customer support and request for the carding software.

STEP THREE: Install/sign into the software to get started.

On step three (3), after you have gotten the carding software, next step is to login, click on the carding button, fill up the card details, enter amount and process. the amount you pulled off that bank account through the linked debit/credit card you stole will be in your wallet on the carding software.

This is the final stage and it is the reason why we mentioned you need offshore bank account or DEX crypto wallet, the reason for this is to clean the funds. Now you will either choose to withdraw the money to your Dex crypto wallet or to the offshore bank account.

How Can I Create Dex Wallet?

To create a DEX (Decentralized Exchange) wallet, you typically need a non-custodial wallet to be able to create a decentralised exchange wallet for yourself, kindly learn more here.

If you have any question, do not hesitate to contact us right away and we will help.

Here are 4 steps to create a dex wallet we without breaking sweat, to create a DEX (Decentralized Exchange) wallet, you typically download a non-custodial wallet like MetaMask or Phantom, set it up by securely saving your recovery phrase, and then connect it to DEX platforms like Uniswap or PancakeSwap to start trading, or use an integrated exchange wallet like OKX Wallet or Inflowbit wallet for simpler smart contract-based access, often using passkeys for ease of use and security.

The process involves choosing a wallet, generating your keys, securing your backup, and connecting to dApps.

1. Choose Your Wallet Type

Browser Extension/Mobile App: (MetaMask, Phantom, Trust Wallet) Most common for direct interaction with DEXs.

Integrated Exchange Wallet: (e.g., OKX DEX Wallet) Offers a simplified, smart contract-based experience that uses passkeys for easier management within an exchange ecosystem, often with built-in gas fee solutions.

2. Create Your Wallet

Download: Get the official app or extension from the store or website.

Create New Wallet: Select “Create a New Wallet”.

Secure Your Recovery Phrase (Seed Phrase): This is crucial! Write down the 12/24-word phrase and store it offline (not digitally).

Set Passkey (for some wallets like OKX or Inflowbit.com): Follow prompts to create a passkey for passwordless login, backed up to your cloud (iCloud/Google).

Set Security: Add a PIN, biometric login, or 2FA if available.

3. Connect to a DEX

Go to the DEX: Open a decentralized exchange (like Uniswap on Ethereum, PancakeSwap on BNB Chain) in your browser or app.

Click “Connect Wallet”: Select your wallet type (MetaMask, OKX, etc.) from the options.

Authorize: Approve the connection request in your wallet.

4. Start Trading

Deposit Crypto: Send crypto (like ETH, BNB, SOL) to your new wallet’s address.

Swap Tokens: Use the DEX interface to swap tokens, pay gas fees (sometimes covered by integrated wallets), and manage your trades.

🚨 Most Important 🚨

Verify URLs: Always use official links to avoid scams.

Check Contract Addresses: Confirm token contract addresses before swapping.

Understand Gas: Be aware of transaction fees (gas) on the network you’re using.

That’s all on 4 Steps To Create A Dex Wallet, if you have any questions do contact us right away and kindly share this with your friend who might need it.

Those looking for how to withdraw cash from a credit card without a PIN, here is a solution. Withdraw money from ATM card without PIN or OTP.

One trick to withdraw money from a credit card is that you can use a pay code-enabled ATM to withdraw money from a credit card without a PIN. If this option is available, you can use your card from your mobile app, prompting a QR code for you to scan at the ATM, allowing you to withdraw cash without a PIN.

This nifty feature may or may not be available with your card issuer; verify with them before attempting. However, you can withdraw cash from a credit card without a PIN through advanced carding and for you to perform advanced carding you will need the software, contact us for more info regarding the advanced carding software.

How to get a cash advance on a credit card without a PIN

Need a cash advance but don’t have your PIN? – do not worry. Remember that cash advances have limits depending on your card and the associated fees, so verify this information before completing the cash advance. Once you confirm this information, there are a few ways to get your cash advance without a PIN which i have detailed below 👇

1. Walk into the bank

You can go directly to your bank and ask for a cash advance. You will usually need to go to the teller and present your card and ID. Using this, they will be able to complete the cash advance and get you your cash.

2. Consider using a check

Your credit card company might issue checks automatically when you open your credit card. These checks can be used to get cash from your credit card. You can write the check out for the amount you need, within your limits, and cash it or deposit it into your bank account. If your credit card company did not send them automatically, you could always request them to be mailed, although it could take a few days.

3. Digital payment service

Digital payment services like Venmo and PayPal are great ways to get a cash advance without a pin. Link your credit card to your digital account, and the funds will transfer there automatically. Now you have the funds on hand without the need to withdraw and deposit any cash.

What to do if you forgot your credit card PIN

While all these ways of withdrawing cash without a PIN are available, you should still try to get your PIN number for future transactions. Here are the easy steps to take to get your credit card PIN.

Log onto your online banking portal

Log on to your online banking account with your credit card company. There is likely an option to request a new PIN number. You will need some identifying information such as your credit card CVV, expiration, and in some cases, your full card number. Depending on your bank, you could have the new PIN instantly, or it could be mailed to you.

Call your credit card issuer

You can call your credit card issuer directly to have them send you a new PIN. The process is relatively simple. First, contact customer service; this number can be found online or on the back of your card, and let them know you need a new PIN number.

Your credit card company will ask questions to verify your identity and protect your account. Be prepared with either your credit card number or other identifying information. Then, they will issue a PIN via mail. Expect it to take 7-10 days, but it could come sooner.

No Debit/Credit Card PIN? No Problem!

Don’t have your PIN? Don’t worry; there are still ways to get cash from your credit card without it. First, when considering a cash advance, ensure you know the fees and your cash advance limit. From there, you can enter the branch associated with your account, use a digital payment service, or even write a check.

Finally, call your card company or request one online if you still want a PIN. One little setback doesn’t have to stop you from getting your hands on cash in a time of need.

How can I pull money from my credit card?

You can get cash from your credit card by completing a cash advance. Keep in mind cash advances have different fees and rates than when using it for standard purchases.

Do cash advances on credit cards hurt your credit score?

Not directly. A cash advance does increase your credit card utilization and have higher fees which could make it harder to pay off your card, ultimately affecting your credit score if not maintained.

How can i pull money from someone’s credit card?

To pull money from someone’s credit card you will have to do that through advanced carding using the carding software, learn more here.

10 Ways To Get Cash From a Credit Card Without a PIN Through Carding (Bypassing Security).

Can you use a credit card at an ATM if it doesn’t have a PIN?

Legally on Ways To Get Cash From a Credit Card Without a PIN? No, Illegally on Ways To Get Cash From a Credit Card Without a PIN? Yes, learn more here. If it’s legally, you can go into the branch and request a cash advance from your card. Want to clone debit cards? Check out this platform for Debit/Credit Cards cloning and bank account flashing.

You have paid your suppliers in China or any other country in overseas, but they claim they haven’t received the payment. Meanwhile, your bank confirms that the transaction was processed. Now, you’re left wondering: How do I prove to the suppliers that the payment has already been made?

This is where the MT103 becomes essential. The MT103 is basically your proof of payment that you can use to confirm a transfer, track delays, or resolve a dispute. It shows all transfer details, including when and where the funds were sent. It’s usually used with SWIFT international payments.

In this article, we will explain what the MT103 is, how it works, what information it provides, how to read its fields, and where to find it.

What Is an MT103?

An MT103 (Message Type 103) is a document that contains a message banks use to complete a SWIFT international transfer between one account to another. It is also referred to as an “MT103 Single Customer Credit Transfer.”

An MT103 can be used as proof of payment and is recognised by institutions worldwide. It includes a detailed record of all the standardised information banks used to make transfers and can provide the recipient with transaction details, including any applicable fees and currency exchange rates.

What Can You Use an MT103 For?

You can use the MT103 document

To keep clear payment records: It gives you a detailed and organised record of your international transfer, so you know what was sent and when. This reduces the risk of disputes. A common issue is when the amount received differs from the amount sent, often due to fees deducted by intermediary banks during the transaction. The MT103 can help you track this discrepancy.

As proof of payment: The MT103 acts like an official receipt, confirming that your funds were sent. This can help if you need to resolve any disputes or keep track for auditing purposes.

To track your payment: MT103 comes with a unique reference number, which banks can use to track and verify a payment’s progress if delays or discrepancies occur.

If you are expecting a payment from a client or a refund from a supplier, you can request an MT103. This document confirms that the transfer has been initiated.

Note: An MT103 means that the payment has been initiated and sent, but it does not necessarily mean it has arrived. To confirm where the payment is, you use a unique reference number found on the MT103 and enter it in the bank tracking tools. To get the tracking tool or to have the software and be able to perform PACS008 (MT103) MX SWIFT ISO20022, kindly contact us.

That’s all on PACS.008 [MT103]: ISO 20022 SWIFT MX message Guide, kindly share if you find this article helpful.

Here are 10 Ways To Get Cash From a Credit Card Without a PIn in an emergency situation where you need cash, you will need to consider all options. Getting money from your credit card, also known as a cash advance, is one solution in this scenario.

What About When You Can’t Get Cash Advance? Let’s Discuss!

10 Ways To Get Cash From a Credit Card Without a PIn

Let’s say you don’t have access to your PIN number. Maybe you forgot or never set it up. While you need the PIN to withdraw from an ATM, there are still other ways to get cash from your credit card. We are breaking down a trick to withdraw money from a credit card and how to get cash from a credit card without a PIN.

Can you use a credit card without a PIN?

There is nothing impossible. You might not have your PIN number, but you can still use your credit card without it. Most point-of-sale machines offer contactless pay options where you can wave your card next to the reader.

Contactless pay options allow you to complete your transaction without inserting your card into the machine. Similarly, there are options to pay from your phone. Apps like Apple and Google Pay allow you to use your phone at the card reader by simply scanning it across the card reader.

You typically need to unlock your phone to use this feature in this scenario. If you have Face ID or a passcode enabled, you will need to use either to complete the transaction. Technology has added to the convenience of using your card quickly and with little hassle.

Can I withdraw cash from an ATM without a PIN?

This question will be generally answered, If you need to withdraw cash from an ATM, you must use a PIN. This added security feature ensures that someone cannot access your account if they find your lost card somewhere. However, there are other ways one can withdraw money from an ATM card even without the pin and OTP will be bypassed.

Pay attention!

How to withdraw cash from a credit card without a PIN

One trick to withdraw money from a credit card is that you can use a pay code-enabled ATM to withdraw money from a credit card without a PIN. If this option is available, you can use your card from your mobile app, prompting a QR code for you to scan at the ATM, allowing you to withdraw cash without a PIN.

This nifty feature may or may not be available with your card issuer; verify with them before attempting. However, you can withdraw cash from a credit card without a PIN through advanced carding and for you to perform advanced carding you will need the software, contact us for more info regarding the advanced carding software.

How to get a cash advance on a credit card without a PIN

Need a cash advance but don’t have your PIN? – do not worry. Remember that cash advances have limits depending on your card and the associated fees, so verify this information before completing the cash advance. Once you confirm this information, there are a few ways to get your cash advance without a PIN which i have detailed below 👇

1. Walk into the bank

You can go directly to your bank and ask for a cash advance. You will usually need to go to the teller and present your card and ID. Using this, they will be able to complete the cash advance and get you your cash.

2. Consider using a check

Your credit card company might issue checks automatically when you open your credit card. These checks can be used to get cash from your credit card. You can write the check out for the amount you need, within your limits, and cash it or deposit it into your bank account. If your credit card company did not send them automatically, you could always request them to be mailed, although it could take a few days.

3. Digital payment service

Digital payment services like Venmo and PayPal are great ways to get a cash advance without a pin. Link your credit card to your digital account, and the funds will transfer there automatically. Now you have the funds on hand without the need to withdraw and deposit any cash.

What to do if you forgot your credit card PIN

While all these ways of withdrawing cash without a PIN are available, you should still try to get your PIN number for future transactions. Here are the easy steps to take to get your credit card PIN.

Log onto your online banking portal

Log on to your online banking account with your credit card company. There is likely an option to request a new PIN number. You will need some identifying information such as your credit card CVV, expiration, and in some cases, your full card number. Depending on your bank, you could have the new PIN instantly, or it could be mailed to you.

Call your credit card issuer

You can call your credit card issuer directly to have them send you a new PIN. The process is relatively simple. First, contact customer service; this number can be found online or on the back of your card, and let them know you need a new PIN number.

Your credit card company will ask questions to verify your identity and protect your account. Be prepared with either your credit card number or other identifying information. Then, they will issue a PIN via mail. Expect it to take 7-10 days, but it could come sooner.

No Debit/Credit Card PIN? No Problem!

Don’t have your PIN? Don’t worry; there are still ways to get cash from your credit card without it. First, when considering a cash advance, ensure you know the fees and your cash advance limit. From there, you can enter the branch associated with your account, use a digital payment service, or even write a check.

Finally, call your card company or request one online if you still want a PIN. One little setback doesn’t have to stop you from getting your hands on cash in a time of need.

How can I pull money from my credit card?

You can get cash from your credit card by completing a cash advance. Keep in mind cash advances have different fees and rates than when using it for standard purchases.

Do cash advances on credit cards hurt your credit score?

Not directly. A cash advance does increase your credit card utilization and have higher fees which could make it harder to pay off your card, ultimately affecting your credit score if not maintained.

How can i pull money from someone’s credit card?

To pull money from someone’s credit card you will have to do that through advanced carding using the carding software, learn more here.

10 Ways To Get Cash From a Credit Card Without a PIN Through Carding (Bypassing Security).

Can you use a credit card at an ATM if it doesn’t have a PIN?

Legally on Ways To Get Cash From a Credit Card Without a PIN? No, Illegally on Ways To Get Cash From a Credit Card Without a PIN? Yes, learn more here. If it’s legally, you can go into the branch and request a cash advance from your card. Want to clone debit cards? Check out this platform for Debit/Credit Cards cloning and bank account flashing.

Many people are asking “How Does Carding Work?” While some are looking for a way to bypass OTP and withdraw cash from debit/credit cards, so here is an article that will put you through.

To save you from the long paragraphs of article, we recommend you contact us right away and ask your direct question, otherwise kindly read carefully.

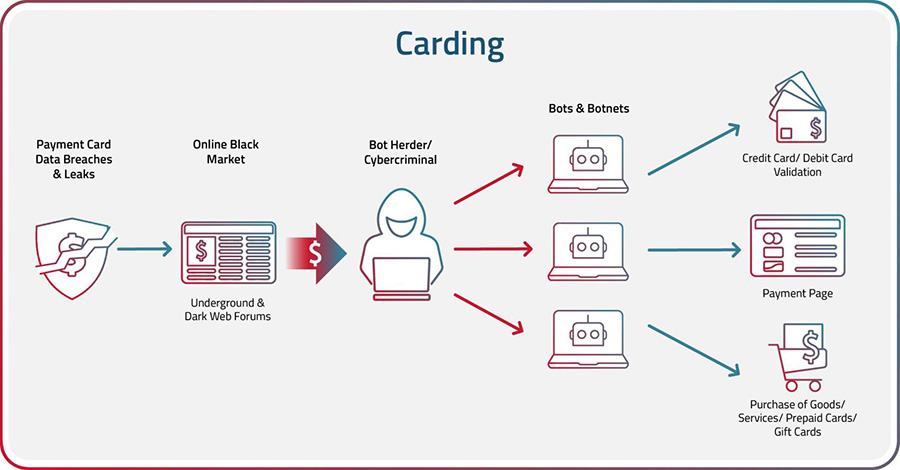

The process of executing a carding attack typically involves several steps:

Obtain Credit/Debit Card Information: Carders obtain credit card information by stealing physical credit cards, purchasing credit card data on the dark web, or using techniques such as phishing, skimming, or malware to steal credit card information. Account Takeover (ATO) of user accounts on e-commerce or financial websites carried out by bots is yet another way for bad actors to steal payment card data.

Validate Card Data: After carders obtain payment card data, they often use bots to validate the cards and check the balances or credit limits on the card with credential stuffing and credential cracking. Credential stuffing is a technique that uses bots to rapidly enter lists of breached or stolen card data to try to validate them. Credential cracking is the process of entering random characters over multiple attempts in the hope of eventually guessing the right combination.

Drop Shipping: A drop is a location where the fraudster can have fraudulently purchased items shipped without revealing their own identity or location.

Make the Purchase: The cybercriminal can use the stolen credit card information to make purchases online or in-store. They may use a technique known as “card present” fraud to create a counterfeit card and make purchases in-person. “Card not present” fraud indicates when the purchase was made online.

Keep or Resell the Goods: Once fraudsters receive the fraudulently purchased items, they will either keep them for personal use or resell them on the black market for cash.

Infographic Stages of Carding

What are the Most Common Carding Attacks?

Phishing: Cybercriminals send a fake email or text message to the victim, posing as a legitimate company. They request that the victim provides their credit/debit card information, which they can use to make fraudulent purchases.

Social Engineering: The fraudster poses as a legitimate representative of a company or financial institution and convinces the victim to provide their credit card information over the phone or through email.

Identity Theft: A thief steals a victim’s personal information, such as their name, address and social security number, and uses that information to open new credit card accounts or make purchases using the victim’s existing credit card.

Malware: Nefarious actors install malicious software on a computer or mobile device to capture the victim’s payment card information when they make online purchases.

Card Skimming: In this type of fraud, criminals use a device known as a skimmer to steal credit card information. The skimmer is placed on a legitimate card reader, such as an ATM or gas pump, and records the card data when the victim swipes or inserts their card.

Already Have The Card Details And Want To Withdraw Money From The Debit/Credit Card Bypassing OTP?

Why going through all the stress outlined on above paragraphs?

Here Is The Real “Advanced Carding” The Solution solution!

Asking “How Does Carding Work?” Is irrelevant because this is a direct guide on how to withdraw money from debit card and convert it to cryptocurrency without trace. Learn more here, for more information contact us right away.

![PACS.008 [MT103]: ISO 20022 SWIFT MX message Guide](https://mt103.org/wp-content/uploads/2025/12/images-79.jpeg)