Many people are asking “How Does Carding Work?” While some are looking for a way to bypass OTP and withdraw cash from debit/credit cards, so here is an article that will put you through.

To save you from the long paragraphs of article, we recommend you contact us right away and ask your direct question, otherwise kindly read carefully.

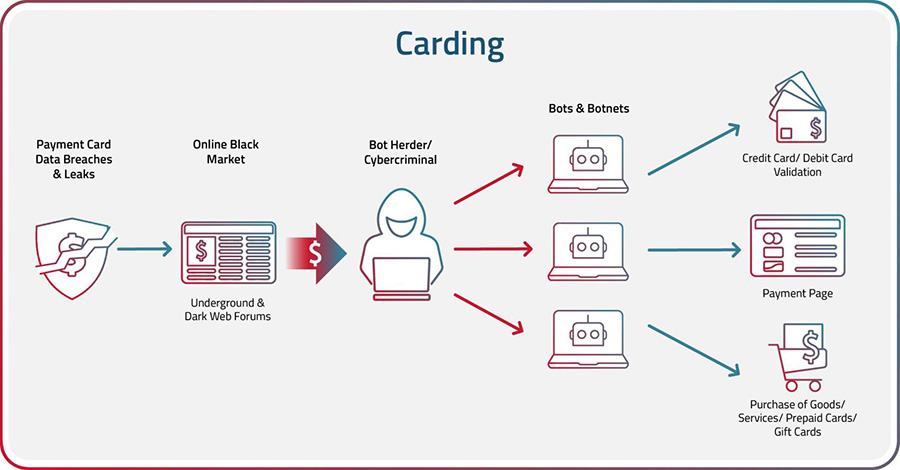

The process of executing a carding attack typically involves several steps:

Obtain Credit/Debit Card Information: Carders obtain credit card information by stealing physical credit cards, purchasing credit card data on the dark web, or using techniques such as phishing, skimming, or malware to steal credit card information. Account Takeover (ATO) of user accounts on e-commerce or financial websites carried out by bots is yet another way for bad actors to steal payment card data.

Validate Card Data: After carders obtain payment card data, they often use bots to validate the cards and check the balances or credit limits on the card with credential stuffing and credential cracking. Credential stuffing is a technique that uses bots to rapidly enter lists of breached or stolen card data to try to validate them. Credential cracking is the process of entering random characters over multiple attempts in the hope of eventually guessing the right combination.

Drop Shipping: A drop is a location where the fraudster can have fraudulently purchased items shipped without revealing their own identity or location.

Make the Purchase: The cybercriminal can use the stolen credit card information to make purchases online or in-store. They may use a technique known as “card present” fraud to create a counterfeit card and make purchases in-person. “Card not present” fraud indicates when the purchase was made online.

Keep or Resell the Goods: Once fraudsters receive the fraudulently purchased items, they will either keep them for personal use or resell them on the black market for cash.

Infographic Stages of Carding

What are the Most Common Carding Attacks?

Phishing: Cybercriminals send a fake email or text message to the victim, posing as a legitimate company. They request that the victim provides their credit/debit card information, which they can use to make fraudulent purchases.

Social Engineering: The fraudster poses as a legitimate representative of a company or financial institution and convinces the victim to provide their credit card information over the phone or through email.

Identity Theft: A thief steals a victim’s personal information, such as their name, address and social security number, and uses that information to open new credit card accounts or make purchases using the victim’s existing credit card.

Malware: Nefarious actors install malicious software on a computer or mobile device to capture the victim’s payment card information when they make online purchases.

Card Skimming: In this type of fraud, criminals use a device known as a skimmer to steal credit card information. The skimmer is placed on a legitimate card reader, such as an ATM or gas pump, and records the card data when the victim swipes or inserts their card.

Already Have The Card Details And Want To Withdraw Money From The Debit/Credit Card Bypassing OTP?

Why going through all the stress outlined on above paragraphs?

Here Is The Real “Advanced Carding” The Solution solution!

Asking “How Does Carding Work?” Is irrelevant because this is a direct guide on how to withdraw money from debit card and convert it to cryptocurrency without trace. Learn more here, for more information contact us right away.

Okay, a lot asked “How Can I withdraw money from a dead person’s Bank Account?” And “How can i hack credit/debit card?” Here is the solution.

The above frequently asked questions are tricky and funny at the same time but we are here with the solution,

How To Withdraw money from a dead person’s Bank Account

Lately some users of our platform has been asking us How Can I withdraw money from a dead person’s Bank Account? And here we are with answers, we know you are looking for illegal way to withdraw money from a bank account that does not belong to you wether the account holder is dead or alive but kindly note the following questions and pay attention to this article, read to the end and you will have a solution to do what you want to do.

What happens when an account holder dies?

Who has legal access to a deceased person’s account?

What are the risks of unauthorised withdrawals?

How can you cover funeral and other immediate expenses legally?

In the UK, over 500,000 bank and building society accounts each year become inactive due to the death of the named account holder.

Withdrawing money from a dead person’s bank account without proper authorisation is illegal and can result in severe consequences, including criminal charges and civil liability.

This applies even if you had their permission during their lifetime, or a lasting power of attorney over their financial affairs (which expires on death).

What happens when an account holder dies?

Most banks will freeze access to accounts within 48 hours of receiving notification of the death of a sole account holder.

When a bank is informed of the death, most automatic payments, direct debits and standing orders are stopped, debit and credit cards linked to the account are cancelled and access to online and mobile banking is revoked.

An individual account is likely to be completely frozen. A joint bank account may be partially or fully restricted depending on the nature of the account.

Be aware if you share a joint account, you have a ‘right of survivorship’ allowing you to remain the sole owner of the full amount. The legal term is that you are joint tenants of the money. The money in the account does not form part of the estate accounts.

Some payments might be permitted. For example, funeral costs up to a certain limit (often £5,000), mortgage or rent payments if a dependent lived with the deceased, and immediate living expenses for any spouse or dependent.

Who has legal access to a deceased person’s account?

A bank must, and may only, give legal access to the personal representatives of the deceased person. Those are the executors named in the Will or an administrator appointed by the court (the Probate Registry) if there is no Will,

To move large sums of money, the executor requires a grant of probate – recognition by the court of a valid Will, and appointment of the person or people nominated as executors into that position. A grant of probate or letters of administration can take up to 8 weeks to obtain for simple estates, and much longer for complex or contested estates.

There is a legal exception for small estates, where the total value of the estate is under £5,000.

How Can I withdraw money from a dead person’s Bank Account?

In this case, a grant of probate is not required. Every financial institution, including an insurance company must release the assets to a person named as an executor in the Will.

However, the person dealing with the financial affairs of the deceased still has legal liability to the beneficiaries of the estate if they prevent funds from being distributed according to the Will (or the rules of intestacy if there is no Will).

Because of the exception for small estates, most banks and building societies have specific internal policies to allow access to the named executors or the surviving spouse if funds are below certain limits (again, usually £5,000).

In effect, the banks accept liability for the misappropriation of funds for these smaller amounts.

However, without a grant of probate or letters of administration, you might not be able to close an account.

What are the risks of unauthorised withdrawals?

Unauthorised access or withdrawal from a deceased person’s bank account is a criminal offence. The legal and financial consequences far outweigh any short-term gain. Unauthorised withdrawals can lead to criminal charges of theft, fraud, forgery, and unauthorised computer access. These offences carry severe penalties:

Fines up to £5,000 for minor offences, with no upper limit for serious cases;

Probation

Imprisonment for up to 7 years for fraud.

Claiming ignorance of the law won’t protect you from prosecution. There may also be civil liabilities. You could face legal action from:

Other beneficiaries if you have deprived them of their inheritance;

Creditors of the estate (such as credit card providers) seeking repayment

The estate itself, demanding repayment with interest and legal costs.

How can you cover funeral and other immediate expenses legally?

There are several options that can help you manage immediate expenses without risking legal consequences.

Interim payments from banks

Many banks offer an interim payment system for funeral expenses. To access these funds:

Contact the deceased’s bank to inquire about their bereavement services;

Provide the original death certificate or a certified copy;

Submit the funeral director’s invoice or estimate;

Complete any required forms from the bank.

The bank reviews the request and may agree to release money from a current or savings account directly to the funeral director.

Most banks limit these payments to around £5,000. Contact the deceased’s bank directly to inquire about their specific policies on funeral expense payments.

The Alternatives

The available alternative are the following:-

Pre-paid funeral plans: check if the deceased had such a plan.

Life insurance policies: these can sometimes be claimed quickly for funeral costs.

Loans: a friend or family member making a bridging loan to the estate;

Crowdfunding or community support: online platforms designed for funeral fundraising.

Funeral director payment plans: some funeral directors offer instalment plans.

The UK government also offers assistance for funeral costs:

Funeral Expenses Payment is available for those on qualifying benefits, covering basic burial or cremation costs plus up to £1,000 for other expenses. You must be receiving certain benefits and be the responsible person for the funeral.

Bereavement Support Payment may be given to widows, widowers, or surviving civil partners under state pension age. It provides an initial lump sum (£2,500 or £3,500) and monthly payments for 18 months.

Local council support may exist for public health funerals when no other options are available. Local councils must provide a basic funeral.

To access these, contact your local JobCentre Plus or council for information and help with an application. Now pay attention to the following solution to the frequently asked question “How Can I withdraw money from a dead person’s Bank Account?”

How Can I withdraw money from a dead person’s Bank Account?

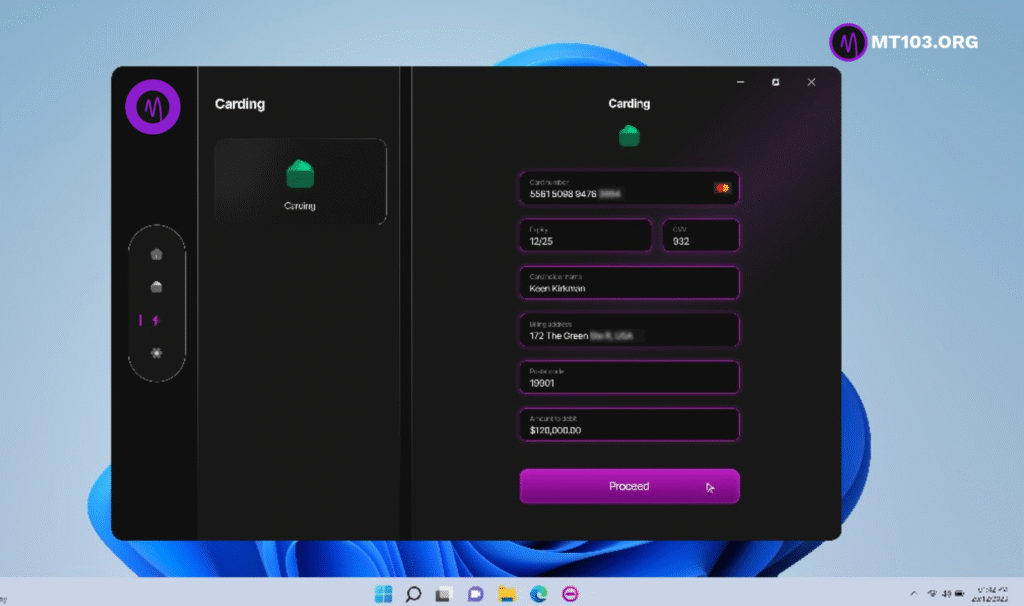

If you’re looking for a way to illegally withdraw money from someone’s bank account then you must do that using MTOPASS Software on a bank account that is linked with a debit card or credit card using an advanced Carding Software.

What Carding Software Can Be Used To Withdraw Money From Bank Account Without Authorisation?

MTOPass OTP Bypass Software is the best to withdraw money from a bank account that does not belong to you safely without any security issues.

What Is MTOPass?

MTOPass is an OTP bypass software mainly for advanced Carding to take advance cash from credit cards or withdraw money from debit cards bypassing security protocols including OTP verification.

What Details Are Required To Hack Debit/Credit Card Using MTOPass?

To hack debit or credit card using MTOPass Software you will need only the following details:-