MT103 Swift Flash Funds Payment With GPI Automatic to carryout seamless MT103, MT202, MT700, MT760, MT799, MT199 and more cash transfer, credit transfer, GPI automatic, IPIP/IPID and DLC with custom CIS.

MT103 SWIFT UETR

MT103 Flash funds system is a software cyber criminals use for Flash funds to carry out fraudulent bank payments for business deals, purchases, goods and services on internet or in person mostly to people that doesn’t know their true identity depending on which criminal and what circumstance of the payment,

Majority of these cyber criminals use this nowadays for P2P payments for digital currencies such as bitcoin, USDT and other digital currencies that are being traded on digital exchanges,

With MT103 flash funds software these criminals are able to make payments of millions of dollars that their victims can never be able to withdraw from the account the money is deposited after some designated duration of time, using this as a weapon to plunge so many businesses into bankruptcy, to this day across over one hundred (100) countries in the world.

Cyber criminals commit bank fraud with this MT103 flash funds software, they can easily send payment of $1,000 and above to any bank account and the beneficiary (their victim) will receive it instantly as local payment or within three (3) business days as swift/foreign wire transfer (cross boarder) payment.

Does Flash Funds reflect on bank account available balance?

This specific flash funds payment these cyber criminals carry out actually reflects on available balance of their victims, the answer to this question is yes. it reflects on bank account available balance,

Breakdown Of Flash Funds Reflection on Bank Account Available Balance

For an example, you are their victim who they have targeted and you already have one hundred thousand dollars ($100,000) in your bank account as current available balance then the cyber criminals sends you twenty thousand dollars ($20,000) to your bank account, upon the arrival of the inward payment inflow to your bank account the current available balance of your bank account will be updated to one hundred and twenty thousand dollars ($120,000). This is how the flash funds reflection on available balance occurs when these cyber criminals initiate the flash funds transaction.

How Cyber Criminals Make Fortunes With Flash Funds

They will engage in a contract or business partnership with their unsuspecting victims, either you’re selling goods, or you’re offering a service, most of them dwell on crypto exchange, they buy crypto currency (a digital asset) and pay with flash funds,

Further BreakDown of How Cyber criminals buy crypto with flash funds

They (buyer) will appear as buyer of your digital asset while some will use it to for other various things and after they pay their victim (seller) of digital which the victim confirms payment has been received and releases the digital asset to the buyer (the cyber criminal) that’s it, whatever issue with payment and withdrawal that comes up next or afterwards is all on the victim to deal with leading to thousands of their victims all over the world losing so much money and going bankrupt.

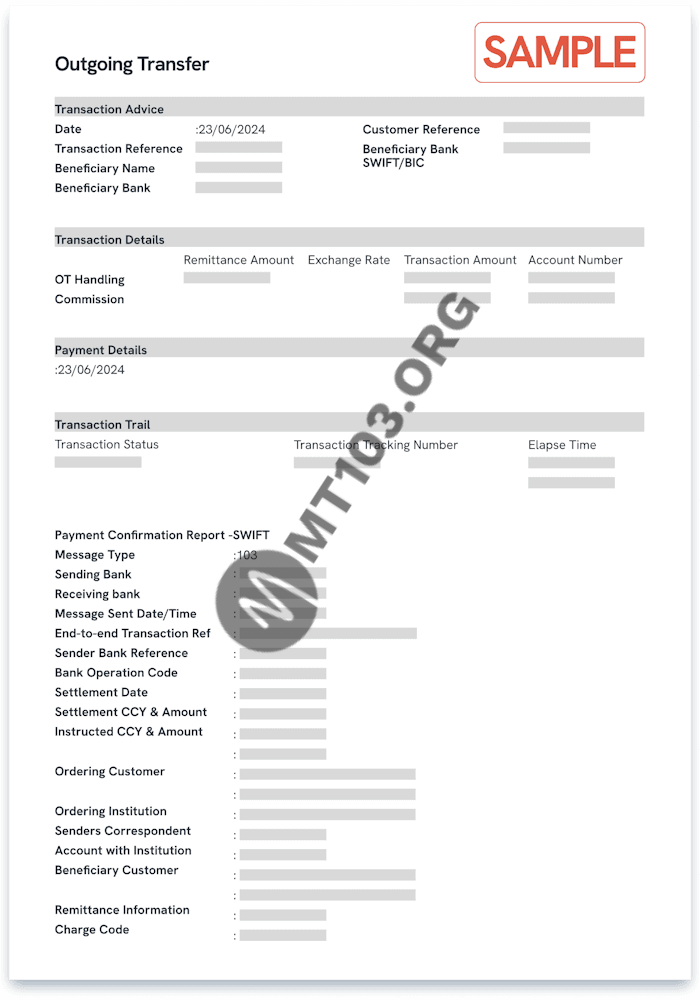

Completed Flash Funds Transaction Snippet

How P2P Digital Crypto Traders Lose Millions To Flash Funds Scams

These cyber criminals will open a trade as buyer of digital asset from their unsuspecting victims on any platform such as Inflowbit, Binance, Kucoin, Paychatik and more, after they open trade to buy Bitcoin or USDT they will then pay their victim (seller of digital asset) which the victim will confirm receiving payment from the cyber criminal and releases the digital asset to the buyer (cyber criminal) that’s it,

What Happens After That?

whatever happens or issue with the payment and withdrawal that comes up next or afterwards is all on the victim to deal with, this has led many to huge loss all over the world making many of their victims to lose so much money in such wired advanced scam.

After the banking system flags the transaction (Flash funds payment), the transaction will be rejected leading to beneficiary having issue with bank and losing both funds and bank account.

MT103 Swift Flash Funds Payment With GPI Automatic

2 Types of Flash Funds

There are many types of flash funds and they all vary from MT103 type to MT202 type ranging from different methods by wares, it all depends on what the scammer that is targeting anyone/whoever is using,

Types of Flash Funds Break Down:

- Local Payment (NIP/INTER-Bank/National): local payment is when you pay to someone in South Africa and you are also living in South Africa, then you want to pay the person (local payment). In this case, the flash funds will reflect instantly after it’s initiated by you.

- Cross Boarder Payment: cross boarder payment is when you live in India or any other country in the world and you want to pay someone in Australia, it can be tagged “Swift Payment”, in this case, the flash funds payment will not reflect instantly because it is a cross boarder payment. It will take 2 to 3 business days to arrive to receiver bank account available balance.

Most of this scammers in P2P use this, set this payment, configure it using the swift flash funds payment software.

Security Of Flash Funds

Most of these criminals don’t use security for it while some does, depending on the particular software the criminal is using because some of these softwares they use are built with security as one of the priorities for these cyber criminals.

If you are an active P2P crypto trader/user you must have encountered a situation whereby someone buys digital asset from you and paid, afterwards bank blocks your bank account and tagged it “suspected of fraudulent activity” or the payment you actually confirmed by yourself with your very own clear eyes is no where to be found anymore in your account, if you’re experienced crypto trader you must have experienced this.

If you have experienced it, there’s ninety nine percent plus probability that the person is a scammer and whoever the person was used flash funds software to pay you, most of the Fake bank alert apps they use can be found on public domains while the flash funds softwares are not found on public domains.

Where Does Cyber Criminals Get Flash Funds Softwares?

We have no much idea, from the little we know and from our team’s research so far, I can only list few platforms they use;

FlashFunds.co (FFCO) – this software gives cyber criminals more ability to do more harms to innocent unsuspecting victims of their malicious activities such flash funds (flashing money that will reflect on the bank account available balance of their victims), taking out money from people’s cards, hacking, cloning and many more.

Most of these scammers use this that comes with offshore account to receive payments, learn more here on how scammers use offshore bank account to receive payments from abroad and understand how to play safe, They’re able to receive fraudulent payments from their victims or scams partners from abroad using offshore bank account because it provides them offshore bank accounts for them to use,

Do they have full access to the offshore bank accounts?

Yes, they do have full access to the accounts such as internet banking and mobile app banking, pin, password and e-mail address. whenever they receive payment to these accounts they mostly use it to buy digital assets such as Bitcoin or USDT stable token while some will transfer it and use it as they please.

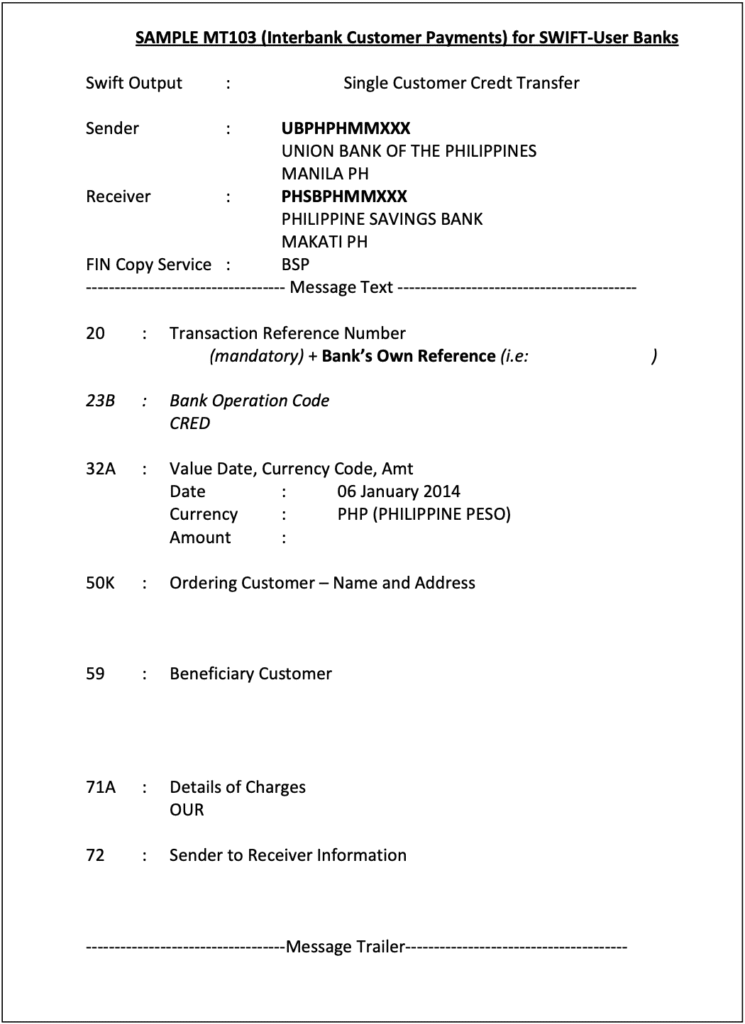

How MT103 Swift Flash Funds Works

The flash funds with encryption is a way of scrambling payment so that the banking system can only verify the authencity of the payment after a designated time frame. The banking system will process the payment in hibernation but will intercept it when the designated time frame has elapsed. In this way, the payment will be rejected and user balance will not remain updated.

The MT103 flash funds payment system works by establishing payment in an encryption flow between the beneficiary banking system and the MT103 flash funds server. (MFFS often use the JOIPsc or SVVER/PYTT protocols.) All outflows from the system are to be checked of authencity after designated timeframe,

Does Flash Funds Require VPN?

It has an inbuilt VPN security and it is highly recommended to turn off all VPN or securities on computer the software is running on, the VPN connections remain private. Imagine josh paying itrona from Canada to Holland using his MT103 flash funds software, the VPN connects automatically so that he can infiltrate the beneficiary bank server that is in a foreign land away. Suppose all of his payments to the beneficiary, as well as the database’s responses, travel through an intermediate Internet exchange point (IXP).

MT103 Swift Flash Funds Payment With GPI Automatic

Now suppose that the criminal (Josh) has already infiltrated this IXP and his payment is passing through a secure connection because of the VPN. All the bank can see is an inflow and will record it because banking system works with records and this inflow is incoming in an encrypted mode that can’t be detected but after the designated time frame the inflow (payment) will be rejected and tagged failed or user account will be deemed (engaging in fraudulent activity) which will be a move for the bank to block the account terminating future risks.

Flash Funds using the MT103 Payment System is not limited to only flashing money into bank account available balance, it can also be used to funds your sports betting account, the following screenshot of a sports betting account funding got flagged and rejected by the banking system after a designated time.

Click Here To Get The Software And Get Started Performing Your MT103 Swift Flash Funds Payments.

This article on MT103 Swift Flash Funds Payment With GPI Automatic is subject to expansion and will be expanded in the future.