Learn the importance Of MT103, How to Get MT103 SWIFT and where to get MT103 SWIFT payment software, whether you’re an exporter, freelancer, or business owner dealing with cross-border transactions, one document that often comes up in event of an international payment that seemed to have vanished is the SWIFT MT103.

SWIFT MT103: Importance Of MT103 And How to Get MT103 SWIFT

Class the MT103 as the digital receipt for your international wire transfer – a standardised SWIFT message issued by the sender’s bank that includes key details of the transfer,

It shows information like the sender, recipient, amount, currency, and reference numbers, plus any charges applied along the way. In other words, it’s a globally recognised proof of payment for SWIFT transactions.

GET THE MT103 SWIFT PAYMENT SOFTWARE NOW!

On this article, you will be guided through what a SWIFT MT103 message actually is, why it matters (especially when payments are delayed or under dispute), how to get one from your bank, and how it can help you track down an international transfer if something goes wrong.

We will also show you how MT103.ORG software that most banks use make tracking international payments easier by saving you time.

What is SWIFT MT103 ?

An MT103 is a standardised SWIFT message format used by banks to confirm that an international wire transfer has been sent. It’s essentially the SWIFT payment confirmation message for a cross-border transaction – kind of like a digital receipt that travels with your money through the banking system. In SWIFT terminology, MT103 is known as a “Single Customer Credit Transfer” message type.

When you send money internationally through the SWIFT network, your bank generates an MT103 message and shares it securely with the recipient’s bank. This SWIFT MT103 document contains all the essential transaction details, including:

- Sender’s information: Your name, account number, and sending bank details.

- Recipient’s information: The beneficiary’s name, account number, and receiving bank details.

- Amount and currency: The exact amount sent and the currency used.

- Date and time: When the transaction was initiated.

- Bank identifiers: SWIFT/BIC codes of both the sending and receiving bank.

- Reference numbers: A unique transaction reference (and UETR, the Unique End-to-End Transaction Reference in newer systems) for tracking.

- Charges applied: Details of any fees or charges deducted (who paid the fees – sender or recipient).

Banks use the MT103 message to track and trace international payments, especially if there’s a delay or a dispute. After your payment is sent, you can request a copy of the MT103 from your bank as evidence that the transfer was processed.

MT103 vs. Other SWIFT Message Types: You might have heard of MT202, which is another SWIFT message. To clarify, MT103 is used for customer payments (it carries all the customer and transaction details as described above), whereas MT202 is a bank-to-bank transfer message used for moving funds between banks (often to settle or cover an MT103).

SWIFT MT103: Importance Of MT103 And How to Get MT103 SWIFT

In simpler terms, if you, as a customer, send money abroad, the transaction is sent as an MT103, and behind the scenes, banks may use an MT202 for their interbank settlement. MT202 messages don’t include customer details, while MT103 messages do. This distinction is mainly important for bankers, but it’s good to know that an MT103 is the document you (or your client) would need as proof of payment in a customer transaction.

What is MT103 SWIFT document used for?

While an MT103 is not required for every international payment, it can be incredibly helpful, especially when you’re sending or receiving large sums or if something goes wrong. Here’s why the MT103 matters:

MT103 SWIFT Proof of Payment

Think of the MT103 as your official receipt for a SWIFT transfer. If you’re the sender, you can share it with your beneficiary or client to confirm that the payment has been made. If you’re the recipient awaiting funds, receiving an MT103 copy verifies that a payment is on the way (not just “in process”) and shows details like the amount and date, which can be crucial for trust and record-keeping.

MT103 SWIFT Easy Tracking

If your money’s stuck or delayed somewhere in transit – especially at an intermediary bank – the MT103 helps your bank trace the transfer. It shows which banks the payment has passed through and where it currently is. Every MT103 comes with a unique transaction reference (Field 20, and a UETR in many cases) that acts like a tracking number. Your bank can use this to query the SWIFT network and find out if the payment is still with the sender’s bank, en route via an intermediary, or delivered to the recipient’s bank.

- Fewer Misunderstandings: Because MT103 follows a global standard, every bank in the SWIFT network understands the format. This standardisation makes it easier to resolve issues and miscommunications. All the information is clearly laid out, which keeps communication between international banks consistent. If there’s a dispute or inquiry, banks refer to the MT103’s details rather than relying on informal messages or emails.

- Compliance and Documentation: Banks and businesses also use MT103 copies for compliance purposes. An MT103 provides a verifiable trail of a payment, which can be used for auditing or to satisfy regulatory requirements. For example, it helps with Anti-Money Laundering (AML) checks by showing where funds came from and where they went. It’s essentially a transparent record of the transaction, which is important for the integrity of the financial system.

Imagine you’ve paid an overseas supplier, but they claim the funds haven’t arrived. You check with your bank, and they confirm the SWIFT transfer was sent – now you’re stuck in the middle, unsure who to believe. This is where the MT103 comes in. By obtaining the MT103 document, you get a detailed record of the payment showing when and where the money was sent, and through which banks.

You can forward this to the beneficiary as proof of payment, and your bank can use the reference information in the MT103 to help trace the payment’s path and find any bottlenecks in the process. Often, just providing the MT103 to the beneficiary’s bank is enough for them to locate a pending credit in their system.

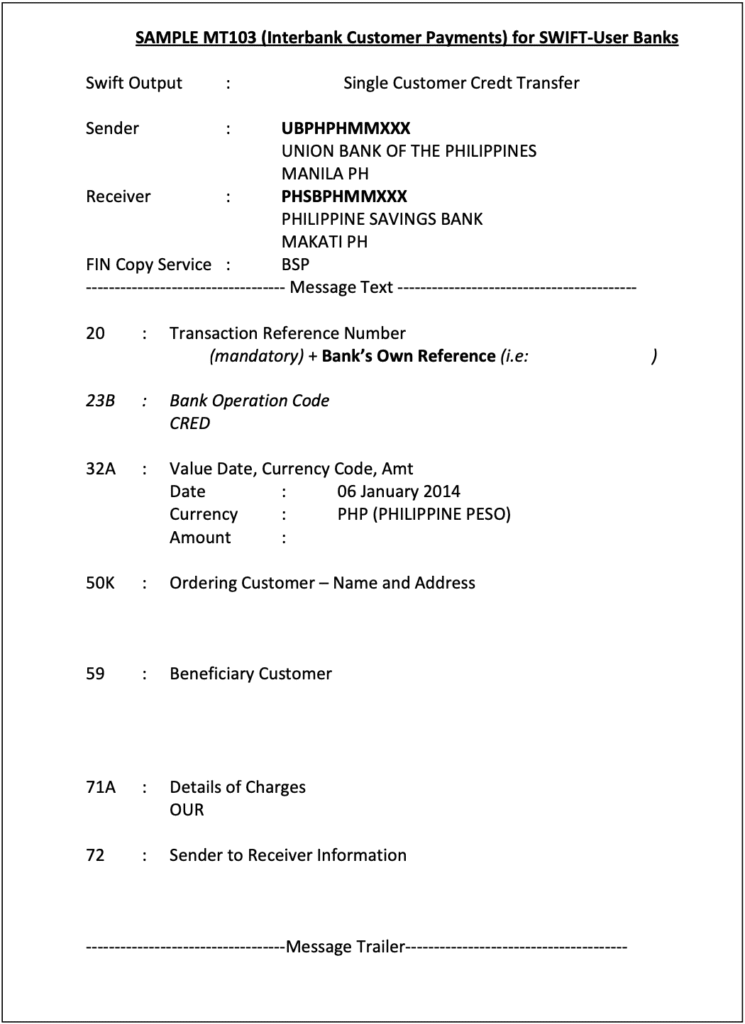

MT103 SWIFT Format and Fields

An MT103 message contains various coded fields that together provide all the transaction information in a structured format. If you’ve never seen one, an MT103 looks a bit cryptic at first – it is a series of lines with codes and values. But each code (or “tag”) corresponds to a specific piece of information.

An MT103 includes all the details necessary for processing an international transfer. Here’s what a typical MT103 message contains:

- Payment Reference (Tag :20:) – A unique identifier for the transaction, assigned by the sending bank. This is the reference number that helps track the payment.

- Date, Currency, and Amount (Tag :32A:) – The value date (execution date of the transfer), the currency, and the amount that was settled.

- Ordering Customer (Tag :50a:) – The sender’s details (name, address, and account number). “50A” or “50F” variants may be used depending on format, but essentially, this is the payer information.

- Beneficiary Customer (Tag :59a:) – The recipient’s details (name and account number/IBAN). This field confirms who is supposed to receive the funds.

- Sending Bank (Tag :52A:) – Identifies the sender’s bank (sometimes included if a different bank is actually initiating on behalf of the sender).

- Intermediary/Correspondent (Tags :53:, :54:,:56:) – These fields (if present) indicate any intermediary banks involved. For example, Tag 56A might show an intermediary bank’s BIC if the payment was routed. These are crucial for tracing delays, as they show the route.

- Remittance Information (Tag :70:) – A reference or description for the payment (often an invoice number or payment purpose text entered by the sender). This is important for the recipient’s reconciliation.

- Details of Charges (Tag :71A:) – Specifies who bears the transfer fees. It will be one of OUR, BEN, or SHA. OUR means the sender pays all fees, BEN means the beneficiary pays all (deducted from the amount), and SHA means fees are shared (each party pays their bank’s fee). For example, if you agreed with your client that you’ll cover transfer costs, the MT103 will show 71A:OUR. (It’s wise for senders and receivers to agree on this beforehand to avoid confusion.)

All this information in the MT103 ensures that the transaction flows smoothly and reaches the right destination with clarity on who paid what. The standardised format means that no matter which banks are involved, the information is structured in a way they all understand.

Every MT103 has specific field tags as outlined above, and learning to read them can be useful. You don’t need to memorise every code, but knowing the key fields helps.

For most users, the critical things to check on an MT103 copy are:

- The transaction reference number (to track it)

- The dates and amount (to confirm timing and amount sent),

- The beneficiary details (to ensure the money was directed to the correct account), and

- The charges field (to see if any fees were taken out).

Mandatory Vs Optional Fields: Some fields appear on every MT103, while others are optional or used only in certain cases. We covered the common mandatory fields (like 20, 32A, 50, 59, 71A, etc.). Optional fields can include:

- Time Indication (Tag :13C:) – Timestamps for various processing events (e.g. time of sending and receiving).

- Transaction Type Code (Tag :26T:) – Indicates the purpose of the transaction (salary, trade payment, etc.) if provided.

- Exchange Rate (Tag :36:) – If currency conversion was involved, the rate can be indicated here.

- Sender to Receiver Info (Tag :72:) – Free-format text for any additional instructions from the sending bank to the receiving bank (often used for things like regulatory info or special notes).

These optional tags might not appear on every MT103, but they offer flexibility to include extra details when needed. For example, a Tag 72 might carry a note like “/INS/ intermediary bank fees to be charged to sender,” or other instructions that don’t fit in the standard fields.

How Do I Get a SWIFT MT103 from My Bank?

If you’ve made a SWIFT transfer and need proof that the payment was sent, the MT103 is what you’re looking for. However, banks do not automatically give out the MT103 document for every transfer – you usually have to request it. Here’s how to get an MT103 from your bank, step by step:

- Make the Transfer: First, you must have made an international payment via SWIFT. An MT103 is automatically generated in the banking system whenever a SWIFT transfer is initiated. It’s not created on demand; it’s created at the time of payment. But it remains behind the scenes unless someone retrieves it.

- Contact Your Bank’s Support: After the payment is sent, reach out to your bank’s customer service (e.g., via phone or through your online banking message center) and request a copy of the SWIFT MT103 for your transaction.Some banks have a dedicated option to request a “SWIFT payment confirmation” or “SWIFT MT103 copy” in their online banking portal – check if that’s available. If not, speaking to a representative or visiting a branch works too.

- Provide Necessary Details: The bank will need to locate the exact transaction, so be ready to provide details such as the date of the transfer, the amount, the currency, and the recipient’s account details. If you have a transaction reference or confirmation number from when you made the transfer, that’s very helpful to give them.

- Wait for the MT103 Document: It can take anywhere from a few hours up to a few days for the bank to retrieve and send you the MT103. The timeframe varies by bank – some can generate it quickly via their system, while others might escalate the request internally. Also, be aware that some banks charge a fee for issuing an MT103 copy. Typically, this fee varies, though it could be higher in some cases. The bank will usually email you the MT103 as a PDF document, or in some cases, provide a physical copy at a branch.

- Receiving the MT103: Once you get the MT103, keep it secure. It contains sensitive information (your name, account number, etc., as well as the beneficiary’s details). It’s generally safe to share with the transaction counterparties (like your beneficiary) since it’s essentially a receipt, not a password or key – but still treat it as a confidential financial document. When you receive it, you can forward it to the beneficiary or the intermediary who needs it as proof.

Important: If you are the receiver of the payment (i.e., waiting for money to come in), note that you usually cannot request the MT103 directly from the sending bank. Only the sender (the bank whose customer sent the money) can issue the MT103.

So if you’re waiting on funds that seem delayed, you should ask the sender (your client or business partner) to request the MT103 from their bank and share it with you. Many times, this comes up if you’re trying to track a missing payment – you’ll have to loop in the sender to obtain the MT103.

In some countries, the MT103 might be referred to by a different name. For example, in India, some banks might call it a “SWIFT Advice” or “SWIFT Copy” instead of using the code “MT103” – but it’s the same document. Don’t be confused by terminology; just clearly ask for proof of the SWIFT transfer or a SWIFT payment confirmation document if the bank seems unsure.

When should you request an MT103?

Since some banks charge for it and it can take effort to obtain, it’s best to request an MT103 only when you need it. Good scenarios are: a payment is significantly delayed or stuck with an intermediary bank, you need the MT103 for compliance documentation or audits, or the beneficiary is insisting on proof to investigate a missing transfer. If everything went smoothly and the beneficiary already got the money, you typically wouldn’t bother getting an MT103 (your regular bank statement or transfer confirmation would suffice in that case).

Who Can Request an MT103?

Generally, the sender of the international payment is the one who can request the MT103 from their bank. The MT103 is generated by the sending bank and is considered that bank’s record of the transaction, so they usually will release it only to their account holder (the sender).

If you are the sending customer, you have the right to ask your bank for the MT103 as proof of payment. If you’re a business and you initiated a wire transfer through your corporate bank account, you (or your finance team) can similarly request the MT103 from your banking relationship manager or through support channels. It doesn’t matter if it’s a personal transfer or a company transfer – the account holder (sender) can obtain it.

If you’re the recipient waiting on a payment, you cannot directly get the MT103 from the sender’s bank. You’d have to ask the sender to do it on their side.

This sometimes causes frustration in international deals, because the receiver might want to independently verify a payment. But due to privacy and banking rules, the receiving bank won’t issue an MT103 for an incoming payment (they can trace it if they have details, but the formal MT103 comes from the sender’s side). So, it often becomes a part of business workflows: the recipient asks the sender to provide the MT103 for reassurance or tracking.

One tip for businesses: If your company sends wires frequently, you might want to set up a process with your bank where they automatically send you the SWIFT confirmation for each transfer. Some banks can arrange to email you the MT103 for every outgoing payment (especially if you have a premium account or use SWIFT a lot). This can save time if proof is often required in your line of work.

How to Track a SWIFT Payment Using MT103

International wire transfers via SWIFT can sometimes take longer than expected – typically 1-5 business days, but delays happen if funds are routed through multiple correspondent banks or if there are compliance checks. If your payment hasn’t arrived within the usual timeframe (say, it’s been a week and still no credit on the other side), it’s natural to want to track where the money is. This is where the MT103 becomes extremely useful: it’s like a tracking slip or a package tracking number for your money.

Using the MT103 Reference to Trace Your Payment: Every MT103 document includes a unique transaction reference code (in Field 20) and often a UETR (Unique End-to-End Transaction Reference) if the transfer was sent through the SWIFT gpi system. Think of this as your payment’s tracking ID.

Once you or your bank has this code, your bank can enter it into the SWIFT tracking systems to check the status of the payment. They can see timestamps of when it left your bank, and if the payment went through SWIFT’s newer GPI (Global Payments Innovation) service, they might even see real-time updates of its journey. For example, SWIFT gpi can show that the payment is “In transit – at intermediary bank in New York” or “Credited to beneficiary bank – pending beneficiary account credit,” etc., in near real-time.

Many major banks now participate in SWIFT gpi, which means they provide status updates for cross-border transfers. Some banks offer customer-facing portals for this tracking, while others will relay the information if you contact support.

Without SWIFT gpi, even with a regular MT103, banks can still perform a SWIFT trace: they send a query or use the reference to see logs of where the payment last was. It’s a bit more manual, but still effective in pinpointing a stuck transfer. The MT103 essentially provides the data needed (like the transaction reference and routing information) to start that investigation. Learn how to Track a SWIFT Payment Using MT103.ORG here.

MT103 VS SWIFT gpi – What’s the Difference?

It’s worth noting that SWIFT gpi is a newer initiative to modernise cross-border payments. MT103 is a message (a document) confirming the payment was sent. SWIFT gpi, on the other hand, is a tracking system/network upgrade that allows end-to-end visibility in real time.

If we use a courier analogy, MT103 is like your shipment receipt and tracking number, whereas SWIFT gpi is the online tracking system you plug that number into, to see exactly where the package (payment) is. Many banks now embed the UETR from SWIFT gpi into the MT103 message itself, learn the difference between MT103 and SWIFT gpi here.