You can not be able to bypass OTP if you don’t learn How to Bypass OTP Verification. Hack Credit/Debit cards. Otp verification are mostly verifications required by an institution or organisation mainly financial institutions as a form of signature to sign and approve a transaction, it is more of a way to verify you are truly the account holder.

On the other hand, other organisations that are not ‘financial institution’ may also require an OTP verification, now for people especially cybercriminals that are looking for ways to break into bank account that does not belong to them and withdraw money without authorisation, they are looking for a way to bypass OTP verification for them to achieve their plan of pulling out money from that account.

This is why on this article, we have laid down a thorough guide for you to learn how to bypass otp verification effortlessly without any risk.

Before we begin, have in mind there are different types of OTP verifications which we have listed below 👇

Types Of OTP Verifications

Text message OTP verification

Email OTP verification

Phone call OTP verification

How OTP Verification Works

OTP verification types fall into algorithmic categories like TOTP (Time-based, common in apps) and HOTP (Counter-based), and delivery methods such as SMS/Email OTPs, Authenticator Apps, and Hardware Tokens, all serving as a second layer of security (2FA/MFA) for logins and transactions by providing temporary codes. One must also understand how the algorithmic works as it is part of learning how to bypass otp verification.

OTP Verification Algorithmic Types (How codes are generated)

TOTP (Time-based One-Time Password): Generates codes that change every 30-60 seconds, synced with a shared secret and the current time; used by Google Authenticator.

HOTP (HMAC-based One-Time Password): Event-based; the code changes with each login attempt or token press, based on an incrementing counter and a shared secret key, not time.

OCRA (OATH Challenge-Response): A challenge-response system where the server sends a challenge (like a random number) and the user’s device responds with a time-bound OTP.

OTP Verification Delivery & Method Types (How you receive the code)

SMS OTP: Code sent as a text message to your phone.

Email OTP: Code sent to your registered email address.

Authenticator Apps: Apps (like Google/Microsoft Authenticator) generate TOTP codes directly on your device.

Hardware Tokens: Physical key fobs or USB devices that generate OTPs.

Push Notifications: A prompt sent to a trusted device asking you to approve or deny the login.

WhatsApp OTP: Increasingly used for delivering codes via the WhatsApp messaging platform.

OTP Verification Common Use Cases

Login/Sign-up: Verifying identity during account access.

Transaction Confirmation: Authorizing bank transfers or purchases.

Account Recovery: Resetting passwords securely.

How to Bypass OTP Verification And Withdraw Money From Someone’s Bank Account

If you are looking a wat to bypass OTP verification and withdraw money from someone’s bank account, kindly learn more here or contact us for future inquiries.

Otp verification are sometimes verified via email addresses or even offshore Mobile numbers, which a website or provider can control and take charge for it’s association with other servers to generate an monitor an OTP request

Let’s further discuss what to Bypass OTP Verification really is

Above we have briefly learnt that OTPs are codes, numbers, or digits delivered to a provided number from an operating system, which clearly mean it can be operated, we will not move any inch further let’s explain what it means to bypass an OTP verification

This digits password is used to verify a phone number and identify a Smart-ID detectors uses OTP to monitor a session of verification service.

How To Bypass OTP Verification

The process of bypassing this OTP verification step to access any website or app quickly is known as OTP bypass. OTP bypass is about using the fake OTP verification process while visiting any application or website. So for many asking if OTP can be bypassed, the answer is Yes. you can. Kindly contact us for support and further inquiry.

Here are 10 Steps To Clone Credit/Debit Card And Withdraw Money – Bypass OTP, if you are looking for a way to hack someone’s credit/debit card bypassing OTP and withdraw money without traces then search no more. On this post you will be guided and you will learn how to hack credit card or debit card through advanced carding method on this 10 steps to clone credit/debit card we have detailed on this article.

10 Steps To Clone Credit/Debit Card And Withdraw Money – Bypass OTP

Before advanced carding, there was carding and we will explain in details on this article, so pay attention.

What Is Carding?

Carding refers to the illegal activity of using stolen credit/debit card details (numbers, CVVs, expiry dates) to buy goods, often prepaid gift cards, to launder money and cover tracks (through buying of digital products or assets such as cryptocurrency),

Essentially fraudulent use of payment card info. It’s a cybercrime where fraudsters obtain card data, often via data breaches or phishing, and use it for purchases, making it a significant part of online fraud.

How Does Carding Works (Bank Card Fraud)?

Carding works through the following steps:

Data Acquisition: Criminals get card numbers from data breaches, malware, or phishing scams.

Purchase of Goods: They use these details to buy high-demand items (electronics, cryptocurrencies, gift cards) online.

Money Laundering: Gift cards are preferred as they’re harder to trace and can be resold for cash.

Dark Web Marketplaces: Stolen card data is also sold on underground forums.

Stolen Cards Acquisition (How To Buy Stolen Credit/Debit Cards)

There are a great many of methods to acquire credit card and associated financial and personal data. The earliest known carding methods have also included “trashing” for financial data, raiding mail boxes and working with insiders.

Some bank card numbers can be semi-automatically generated based on known sequences via a “BIN attack”. Carders might attempt a “distributed guessing attack” to discover valid numbers by submitting numbers across a high number of ecommerce sites simultaneously.

Today, various methodologies include skimmers at ATMs, hacking or web skimming an ecommerce or payment processing site or even intercepting card data within a point of sale network.[10] Randomly calling hotel room phones asking guests to “confirm” credit card details is example of a social engineering attack vector.

Resale Of Stolen Credit/Debit Cards

Stolen data may be bundled as a “Base” or “First-hand base” if the seller participated in the theft themselves. Resellers may buy “packs” of dumps from multiple sources. Ultimately, the data may be sold on darknet markets and other carding sites and forums.

specialising in these types of illegal goods. Teenagers have gotten involved in fraud such as using card details to order pizzas. On the more sophisticated of such sites, individual “dumps” may be purchased by zip code and country so as to avoid alerting banks about their misuse. Automatic checker services perform validation en masse in order to quickly check if a card has yet to be blocked. Sellers will advertise their dump’s “valid rate”, based on estimates or checker data. Cards with a greater than 90% valid rate command higher prices. “Cobs” or changes of billing are highly valued, where sufficient information is captured to allow redirection of the registered card’s billing and shipping addresses to one under the carder’s control.

Full identity information may be sold as “Fullz” inclusive of social security number, date of birth and address to perform more lucrative identity theft.

Fraudulent vendors are referred to as “rippers”, vendors who take buyer’s money then never deliver. This is increasingly mitigated via forum and store based feedback systems as well as through strict site invitation and referral policies.

Funds from stolen cards themselves may be cashed out via buying cryptocurrency, pre-paid cards, gift cards or through re-shipping goods through mules then e-fencing through online marketplaces like eBay.

Increased law enforcement scrutiny over reshipping services has led to the rise of dedicated criminal operations for reshipping stolen goods. Hacked computers may be configured with SOCKS proxy software to optimise acceptance from payment processors.

Money Laundering

The 2004 investigation into the ShadowCrew forum also led to investigations of the online payment service E-gold that had been launched in 1996, one of the preferred money transfer systems of carders at the time. In December 2005 its owner Douglas Jackson’s house and businesses were raided as a part of “Operation Goldwire”. Jackson discovered that the service had become a bank and transfer system to the criminal underworld. Pressured to disclose ongoing records disclosed to law enforcement, many arrests were made through to 2007.

However, in April 2007 Jackson himself was indicted for money laundering, conspiracy and operating an unlicensed money transmitting business. This led to the service freezing the assets of users in “high risk” countries and coming under more traditional financial regulation.

Since 2006, Liberty Reserve had become a popular service for cybercriminals. When it was seized in May 2013 by the US government, this caused a major disruption to the cybercrime ecosystem.

Today, some carders prefer to make payment between themselves with bitcoin, as well as traditional wire services such as Western Union, MoneyGram or the Russian WebMoney service.

Other Methods Or Related Cyber Frauds

Many forums also provide related computer crime services such as phishing kits, malware and spam lists. They may also act as a distribution point for the latest fraud tutorials either for free or commercially. ICQ was at one point the instant messenger of choice due to its anonymity as well as MSN clients modified to use PGP.

Carding related sites may be hosted on botnet based fast flux web hosting for resilience against law enforcement action. Other account types like PayPal, Uber, Netflix and loyalty card points may be sold alongside card details.

Logins to many sites may also be sold as a backdoor access apparently for major institutions such as banks, universities and even industrial control systems. For gift card fraud, retailers are prone to be exploited by fraudsters in their attempts to steal gift cards via bot technology or through stolen credit card information.

In the context of fraud, using stolen credit card data to purchase gift cards is becoming an increasingly common money laundering tactic. Another way gift card fraud occurs is when a retailer’s online systems which store gift card data undergo brute force attacks from automated bots.

Tax refund fraud is an increasingly popular method of using identify theft to acquire prepaid cards ready for immediate cash out. Popular coupons may be counterfeited and sold also. Personal information and even medical records are sometimes available.

Theft and gift card fraud may operated entirely independently of online carding operations. Cashing out in gift cards is very common as well, as “discounted gift cards” can be found for sale anywhere, making it an easy sale for a carder, and a very lucrative operation.

The Google hacks, popularly known as Google dorks for credit card details, are also used often in obtaining credit card details.

Why go through the stress of carding when you can easily withdraw money from any debit card without trace, take out advance cash from stolen credit cards without any traces using “advanced carding”?

What Is Advanced Carding?

Advanced carding is the modern carding method that allows you to hack any credit or debit card, take out money (cash) without any trace or stress of having the money without any law enforcement hunting for you.

How Does Advanced Carding Work?

Advanced carding in ten easy steps, within 5 minutes you can get done with the process if you do it right or have the necessary details and equipment you need to pull this off, the following are advanced carding steps:

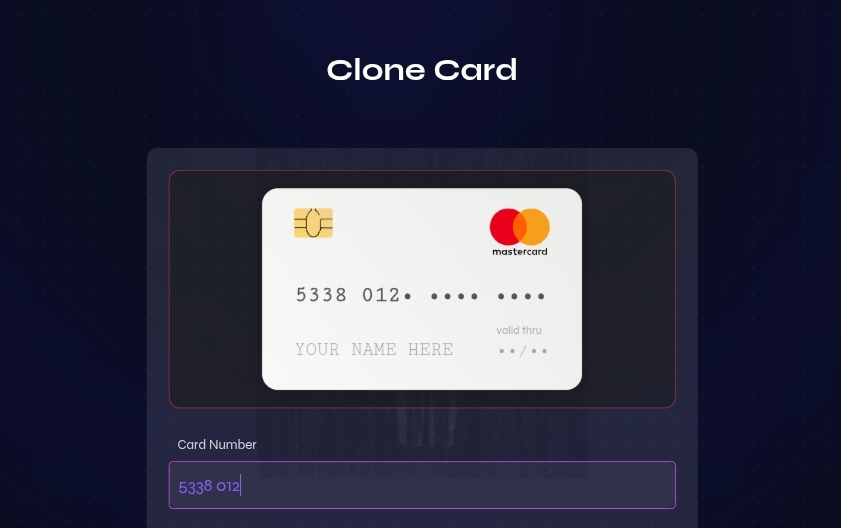

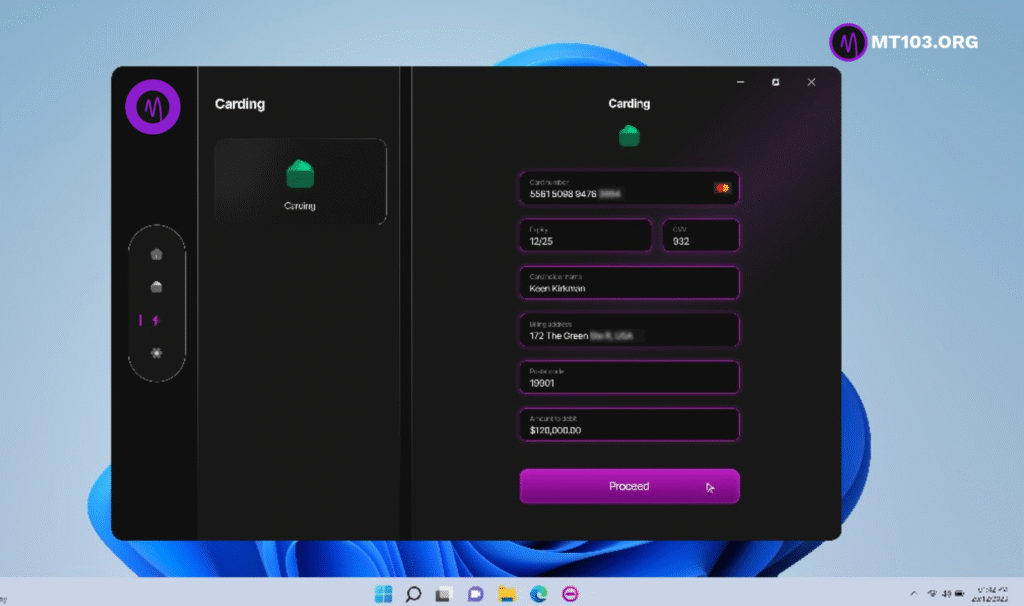

Step 1: get the card info you want to pull or withdraw money from, (required info are Card number, CVV, Expiry date and and card holder’s name. Billing address is optional but we recommend you have it handy).

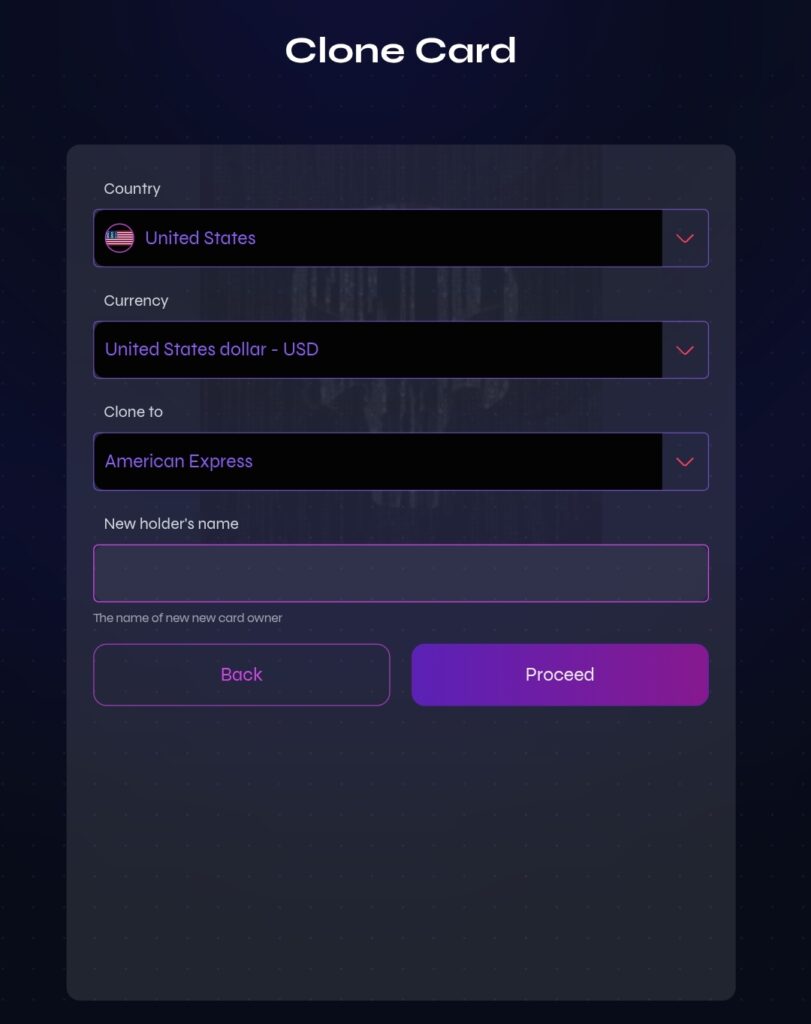

Step 2: Initiate the cloning of the card into a new one, original card will won’t be affected. The cloning process is explained below,

Step 3: Copy the cloned card details and use cardpulling,

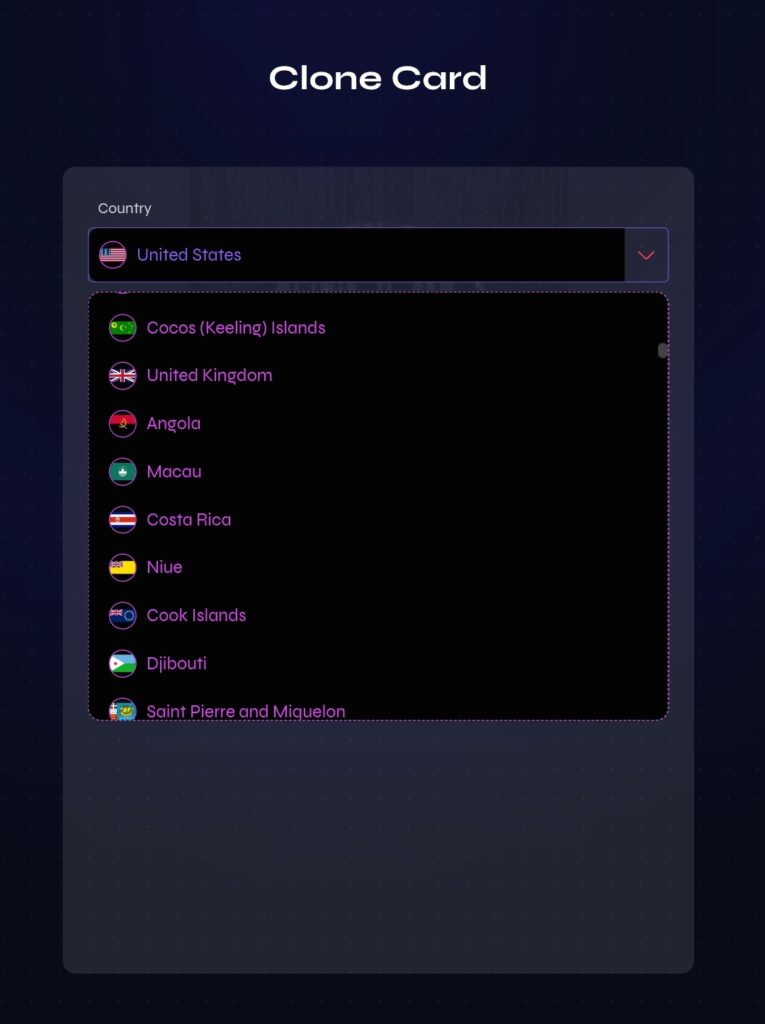

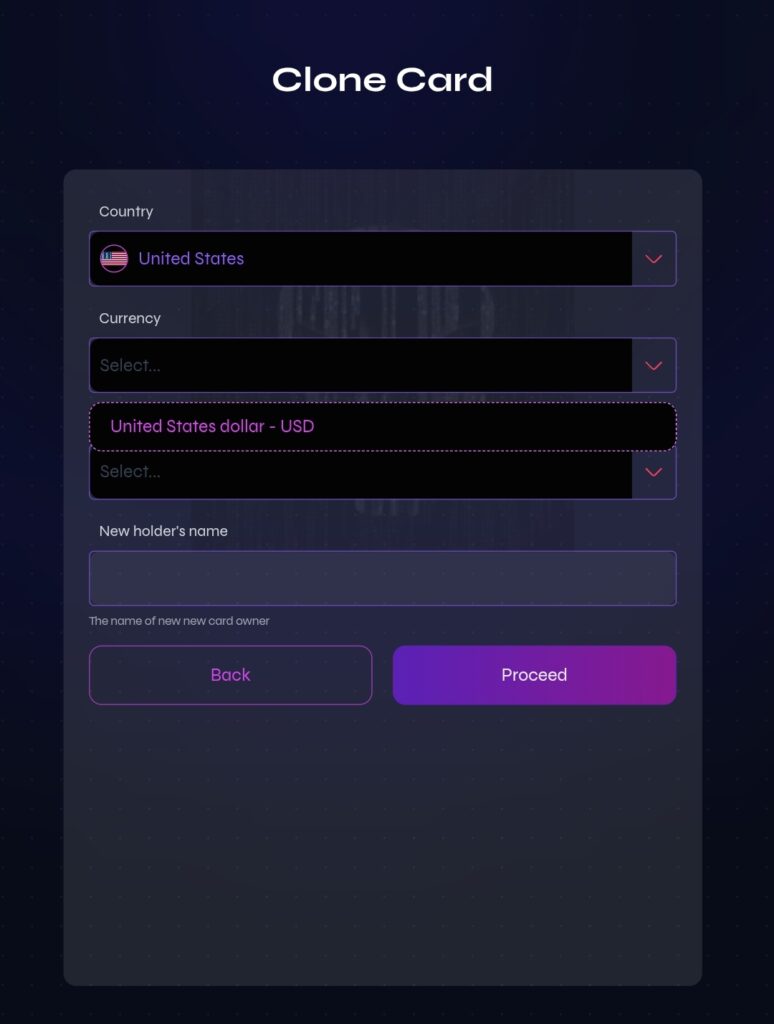

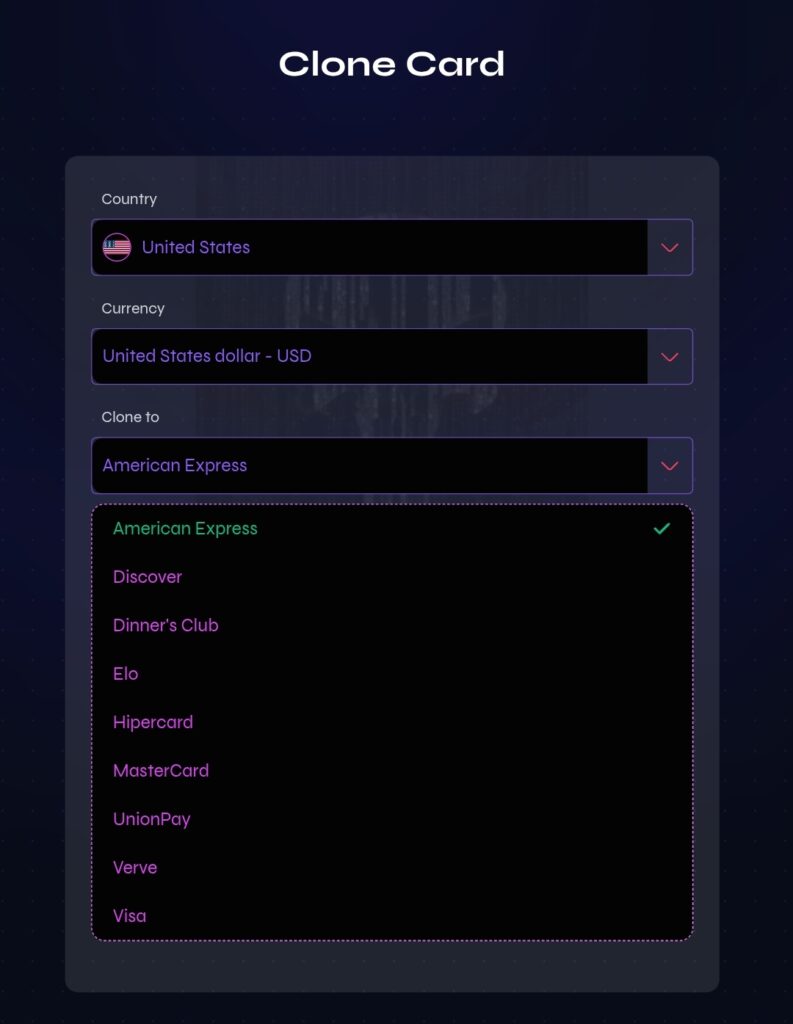

Step 4: choose card type in the cardpulling, choose country and enter card details.

Step 5: Enter amount you want to pull out of the card after entering the card details.

Step 6: Proceed and choose to pull the funds/cash through the dedicated wallet.

Step 7: Pull the money from the card successfully after clicking confirmation button.

Step 8: Head to the wallet, add your crypto wallet address but note that only USDT is recommended for quick confirmation on the network (TRC20, ERC20 and BEP20 networks supported).

Step 9: Head to the convert section, convert the money to usdt crypto (conversion commission applies).

Step 10: Final step, head to the withdrawal section, click withdraw, enter a specific amount or all, choose receiving address, select priority network and click the withdraw button.

The above are 10 Steps To Clone Credit/Debit Card And Withdraw Money Bypassing OTP, also explained in graphic images below, kindly have a look.

STEP ONE (1)

STEP TWO (2)

STEP THREE (3)

STEP FOUR (4)

STEP FIVE (5)

That is all on 10 Steps To Clone Credit/Debit Card And Withdraw Money Bypassing OTP verification, for more info or inquiry kindly contact our support.

MT103 Swift Flash Funds Payment With GPI Automatic to carryout seamless MT103, MT202, MT700, MT760, MT799, MT199 and more cash transfer, credit transfer, GPI automatic, IPIP/IPID and DLC with custom CIS.

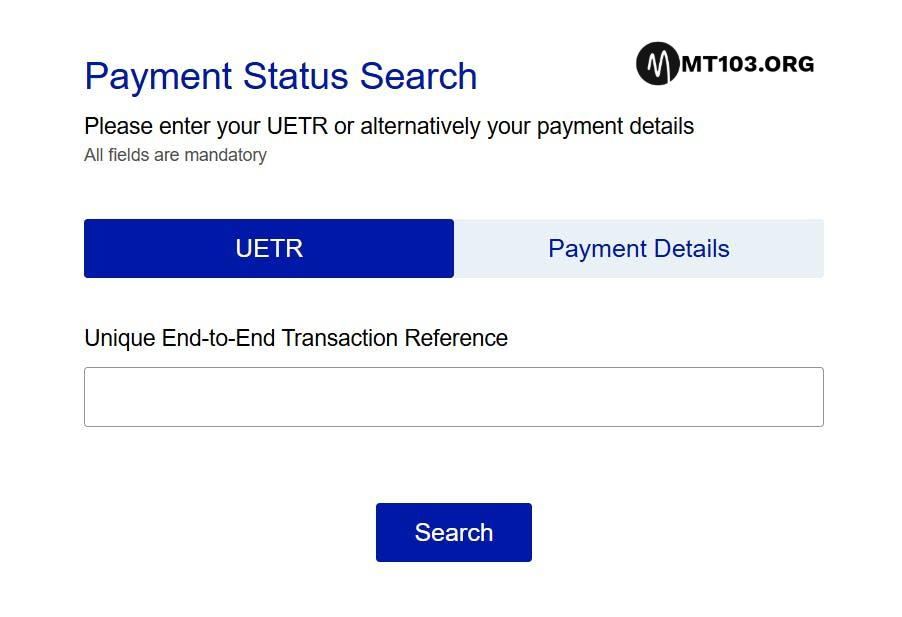

MT103 SWIFT UETR

MT103 Flash funds system is a software cyber criminals use for Flash funds to carry out fraudulent bank payments for business deals, purchases, goods and services on internet or in person mostly to people that doesn’t know their true identity depending on which criminal and what circumstance of the payment,

Majority of these cyber criminals use this nowadays for P2P payments for digital currencies such as bitcoin, USDT and other digital currencies that are being traded on digital exchanges,

With MT103 flash funds software these criminals are able to make payments of millions of dollars that their victims can never be able to withdraw from the account the money is deposited after some designated duration of time, using this as a weapon to plunge so many businesses into bankruptcy, to this day across over one hundred (100) countries in the world.

Cyber criminals commit bank fraud with this MT103 flash funds software, they can easily send payment of $1,000 and above to any bank account and the beneficiary (their victim) will receive it instantly as local payment or within three (3) business days as swift/foreign wire transfer (cross boarder) payment.

Does Flash Funds reflect on bank account available balance?

This specific flash funds payment these cyber criminals carry out actually reflects on available balance of their victims, the answer to this question is yes. it reflects on bank account available balance,

Breakdown Of Flash Funds Reflection on Bank Account Available Balance

For an example, you are their victim who they have targeted and you already have one hundred thousand dollars ($100,000) in your bank account as current available balance then the cyber criminals sends you twenty thousand dollars ($20,000) to your bank account, upon the arrival of the inward payment inflow to your bank account the current available balance of your bank account will be updated to one hundred and twenty thousand dollars ($120,000). This is how the flash funds reflection on available balance occurs when these cyber criminals initiate the flash funds transaction.

How Cyber Criminals Make Fortunes With Flash Funds

They will engage in a contract or business partnership with their unsuspecting victims, either you’re selling goods, or you’re offering a service, most of them dwell on crypto exchange, they buy crypto currency (a digital asset) and pay with flash funds,

Further BreakDown of How Cyber criminals buy crypto with flash funds

They (buyer) will appear as buyer of your digital asset while some will use it to for other various things and after they pay their victim (seller) of digital which the victim confirms payment has been received and releases the digital asset to the buyer (the cyber criminal) that’s it, whatever issue with payment and withdrawal that comes up next or afterwards is all on the victim to deal with leading to thousands of their victims all over the world losing so much money and going bankrupt.

Completed Flash Funds Transaction Snippet

How P2P Digital Crypto Traders Lose Millions To Flash Funds Scams

These cyber criminals will open a trade as buyer of digital asset from their unsuspecting victims on any platform such as Inflowbit, Binance, Kucoin, Paychatik and more, after they open trade to buy Bitcoin or USDT they will then pay their victim (seller of digital asset) which the victim will confirm receiving payment from the cyber criminal and releases the digital asset to the buyer (cyber criminal) that’s it,

What Happens After That?

whatever happens or issue with the payment and withdrawal that comes up next or afterwards is all on the victim to deal with, this has led many to huge loss all over the world making many of their victims to lose so much money in such wired advanced scam.

After the banking system flags the transaction (Flash funds payment), the transaction will be rejected leading to beneficiary having issue with bank and losing both funds and bank account.

MT103 Swift Flash Funds Payment With GPI Automatic

2 Types of Flash Funds

There are many types of flash funds and they all vary from MT103 type to MT202 type ranging from different methods by wares, it all depends on what the scammer that is targeting anyone/whoever is using,

Types of Flash Funds Break Down:

Local Payment (NIP/INTER-Bank/National): local payment is when you pay to someone in South Africa and you are also living in South Africa, then you want to pay the person (local payment). In this case, the flash funds will reflect instantly after it’s initiated by you.

Cross Boarder Payment: cross boarder payment is when you live in India or any other country in the world and you want to pay someone in Australia, it can be tagged “Swift Payment”, in this case, the flash funds payment will not reflect instantly because it is a cross boarder payment. It will take 2 to 3 business days to arrive to receiver bank account available balance.

Most of this scammers in P2P use this, set this payment, configure it using the swift flash funds payment software.

Security Of Flash Funds

Most of these criminals don’t use security for it while some does, depending on the particular software the criminal is using because some of these softwares they use are built with security as one of the priorities for these cyber criminals.

If you are an active P2P crypto trader/user you must have encountered a situation whereby someone buys digital asset from you and paid, afterwards bank blocks your bank account and tagged it “suspected of fraudulent activity” or the payment you actually confirmed by yourself with your very own clear eyes is no where to be found anymore in your account, if you’re experienced crypto trader you must have experienced this.

If you have experienced it, there’s ninety nine percent plus probability that the person is a scammer and whoever the person was used flash funds software to pay you, most of the Fake bank alert apps they use can be found on public domains while the flash funds softwares are not found on public domains.

Where Does Cyber Criminals Get Flash Funds Softwares?

We have no much idea, from the little we know and from our team’s research so far, I can only list few platforms they use;

FlashFunds.co (FFCO) – this software gives cyber criminals more ability to do more harms to innocent unsuspecting victims of their malicious activities such flash funds (flashing money that will reflect on the bank account available balance of their victims), taking out money from people’s cards, hacking, cloning and many more.

Most of these scammers use this that comes with offshore account to receive payments, learn more here on how scammers use offshore bank account to receive payments from abroad and understand how to play safe, They’re able to receive fraudulent payments from their victims or scams partners from abroad using offshore bank account because it provides them offshore bank accounts for them to use,

Do they have full access to the offshore bank accounts?

Yes, they do have full access to the accounts such as internet banking and mobile app banking, pin, password and e-mail address. whenever they receive payment to these accounts they mostly use it to buy digital assets such as Bitcoin or USDT stable token while some will transfer it and use it as they please.

How MT103 Swift Flash Funds Works

The flash funds with encryption is a way of scrambling payment so that the banking system can only verify the authencity of the payment after a designated time frame. The banking system will process the payment in hibernation but will intercept it when the designated time frame has elapsed. In this way, the payment will be rejected and user balance will not remain updated.

The MT103 flash funds payment system works by establishing payment in an encryption flow between the beneficiary banking system and the MT103 flash funds server. (MFFS often use the JOIPsc or SVVER/PYTT protocols.) All outflows from the system are to be checked of authencity after designated timeframe,

Does Flash Funds Require VPN?

It has an inbuilt VPN security and it is highly recommended to turn off all VPN or securities on computer the software is running on, the VPN connections remain private. Imagine josh paying itrona from Canada to Holland using his MT103 flash funds software, the VPN connects automatically so that he can infiltrate the beneficiary bank server that is in a foreign land away. Suppose all of his payments to the beneficiary, as well as the database’s responses, travel through an intermediate Internet exchange point (IXP).

MT103 Swift Flash Funds Payment With GPI Automatic

Now suppose that the criminal (Josh) has already infiltrated this IXP and his payment is passing through a secure connection because of the VPN. All the bank can see is an inflow and will record it because banking system works with records and this inflow is incoming in an encrypted mode that can’t be detected but after the designated time frame the inflow (payment) will be rejected and tagged failed or user account will be deemed (engaging in fraudulent activity) which will be a move for the bank to block the account terminating future risks.

Flash Funds using the MT103 Payment System is not limited to only flashing money into bank account available balance, it can also be used to funds your sports betting account, the following screenshot of a sports betting account funding got flagged and rejected by the banking system after a designated time.

MT103 LOG For Direct Wire Deposit Transfer. Firstly, MT103 is a standardized SWIFT payment message used specifically for cross border/international wire transfers and local payments.

We use SWIFT for all payments made via MT103 swift payment system while MT202 is for inter bank to bank payment which can generally be tagged local payment.

Is MT103 Wire Logs Deposit Globally Accepted?

Our MT103 and MT202 wire LOGs are globally accepted as proofs of payment and include all payment details such as date, amount, currency, sender and recipient.

Can I Be Able To Provide MT103 Or MT202 Proof Of Payment?

Once your payment has been dispatched, you can retrieve your MT103 by logging into your mt103 payment program account, find the completed payment from the history and click ‘View’. Your MT103 will appear at the bottom of the record. There’s even a ‘copy to clipboard’ function so you can forward it to your recipient and option to generate receipt.

Use the table below to view the definition of the MT103 fields;

20

Transaction Reference Number

23B

Bank Operation Code

32A

Value Date / Currency / Interbank Settled

33B

Currency / Original Ordered Amount

50A

Ordering Customer (Payer)

52A

Ordering Institution (Payer’s Bank)

53A

Sender’s Correspondent (Bank)

54A

Receiver’s Correspondent (Bank)

56A

Intermediary (Bank)

57A

Account with Institution (Beneficiary’s Bank)

59

Beneficiary

70

Remittance Information (Payment Reference)

71A

Details of Charges (BEN / OUR / SHA)

72

Sender to Receiver Information

77B

Regulatory Reporting

You will have confirmation that your payment has been sent, including all the important details such as recipient information and payment amount which will serve as a valid proof of payment, whether to send to a supplier to serve as proof of payment or to accounts.

Buy MT103 Direct Wire Deposit LOGs

If you need MT103 Direct Wire Deposit LOGs then do not hesitate to contact us right away today, use any of the below means of contact to reach out to us, tell us the country and amount of log you want.

Looking for MT103 SWIFT? Get it here. Also flash money into any bank account’s available balance or you want Bank Account Available Balance Money Flashing software then you should ensure you get your hands on MT103.ORG Software.

Bank Account Available Balance Money Flashing

Before we proceed further, let’s clarify something, there has been frequent questions being asked by newbies about MT103 Software. Kindly learn more about MT103 here.

Flash Funds Into Bank Account Balance

Users of MT103 Software can do more than MT103 Swift Payments, they can flash funds as well. To flash crypto (USDT and BTC) kindly contact our customer support,

If you want to do carding (hacking of debit or credit cards then we recommend MTOPASS Software, take advance cash from stolen credit cards and withdraw money from debit cards bypassing OTP verifications easily.

How To Get MT103 SWIFT Payment Software

For more info, questions regarding “Bank Account Available Balance Money Flashing” and assistance using the program kindly engage the customer support through email channel or the main chat channel for quick response.

Okay, a lot asked “How Can I withdraw money from a dead person’s Bank Account?” And “How can i hack credit/debit card?” Here is the solution.

The above frequently asked questions are tricky and funny at the same time but we are here with the solution,

How To Withdraw money from a dead person’s Bank Account

Lately some users of our platform has been asking us How Can I withdraw money from a dead person’s Bank Account? And here we are with answers, we know you are looking for illegal way to withdraw money from a bank account that does not belong to you wether the account holder is dead or alive but kindly note the following questions and pay attention to this article, read to the end and you will have a solution to do what you want to do.

What happens when an account holder dies?

Who has legal access to a deceased person’s account?

What are the risks of unauthorised withdrawals?

How can you cover funeral and other immediate expenses legally?

In the UK, over 500,000 bank and building society accounts each year become inactive due to the death of the named account holder.

Withdrawing money from a dead person’s bank account without proper authorisation is illegal and can result in severe consequences, including criminal charges and civil liability.

This applies even if you had their permission during their lifetime, or a lasting power of attorney over their financial affairs (which expires on death).

What happens when an account holder dies?

Most banks will freeze access to accounts within 48 hours of receiving notification of the death of a sole account holder.

When a bank is informed of the death, most automatic payments, direct debits and standing orders are stopped, debit and credit cards linked to the account are cancelled and access to online and mobile banking is revoked.

An individual account is likely to be completely frozen. A joint bank account may be partially or fully restricted depending on the nature of the account.

Be aware if you share a joint account, you have a ‘right of survivorship’ allowing you to remain the sole owner of the full amount. The legal term is that you are joint tenants of the money. The money in the account does not form part of the estate accounts.

Some payments might be permitted. For example, funeral costs up to a certain limit (often £5,000), mortgage or rent payments if a dependent lived with the deceased, and immediate living expenses for any spouse or dependent.

Who has legal access to a deceased person’s account?

A bank must, and may only, give legal access to the personal representatives of the deceased person. Those are the executors named in the Will or an administrator appointed by the court (the Probate Registry) if there is no Will,

To move large sums of money, the executor requires a grant of probate – recognition by the court of a valid Will, and appointment of the person or people nominated as executors into that position. A grant of probate or letters of administration can take up to 8 weeks to obtain for simple estates, and much longer for complex or contested estates.

There is a legal exception for small estates, where the total value of the estate is under £5,000.

How Can I withdraw money from a dead person’s Bank Account?

In this case, a grant of probate is not required. Every financial institution, including an insurance company must release the assets to a person named as an executor in the Will.

However, the person dealing with the financial affairs of the deceased still has legal liability to the beneficiaries of the estate if they prevent funds from being distributed according to the Will (or the rules of intestacy if there is no Will).

Because of the exception for small estates, most banks and building societies have specific internal policies to allow access to the named executors or the surviving spouse if funds are below certain limits (again, usually £5,000).

In effect, the banks accept liability for the misappropriation of funds for these smaller amounts.

However, without a grant of probate or letters of administration, you might not be able to close an account.

What are the risks of unauthorised withdrawals?

Unauthorised access or withdrawal from a deceased person’s bank account is a criminal offence. The legal and financial consequences far outweigh any short-term gain. Unauthorised withdrawals can lead to criminal charges of theft, fraud, forgery, and unauthorised computer access. These offences carry severe penalties:

Fines up to £5,000 for minor offences, with no upper limit for serious cases;

Probation

Imprisonment for up to 7 years for fraud.

Claiming ignorance of the law won’t protect you from prosecution. There may also be civil liabilities. You could face legal action from:

Other beneficiaries if you have deprived them of their inheritance;

Creditors of the estate (such as credit card providers) seeking repayment

The estate itself, demanding repayment with interest and legal costs.

How can you cover funeral and other immediate expenses legally?

There are several options that can help you manage immediate expenses without risking legal consequences.

Interim payments from banks

Many banks offer an interim payment system for funeral expenses. To access these funds:

Contact the deceased’s bank to inquire about their bereavement services;

Provide the original death certificate or a certified copy;

Submit the funeral director’s invoice or estimate;

Complete any required forms from the bank.

The bank reviews the request and may agree to release money from a current or savings account directly to the funeral director.

Most banks limit these payments to around £5,000. Contact the deceased’s bank directly to inquire about their specific policies on funeral expense payments.

The Alternatives

The available alternative are the following:-

Pre-paid funeral plans: check if the deceased had such a plan.

Life insurance policies: these can sometimes be claimed quickly for funeral costs.

Loans: a friend or family member making a bridging loan to the estate;

Crowdfunding or community support: online platforms designed for funeral fundraising.

Funeral director payment plans: some funeral directors offer instalment plans.

The UK government also offers assistance for funeral costs:

Funeral Expenses Payment is available for those on qualifying benefits, covering basic burial or cremation costs plus up to £1,000 for other expenses. You must be receiving certain benefits and be the responsible person for the funeral.

Bereavement Support Payment may be given to widows, widowers, or surviving civil partners under state pension age. It provides an initial lump sum (£2,500 or £3,500) and monthly payments for 18 months.

Local council support may exist for public health funerals when no other options are available. Local councils must provide a basic funeral.

To access these, contact your local JobCentre Plus or council for information and help with an application. Now pay attention to the following solution to the frequently asked question “How Can I withdraw money from a dead person’s Bank Account?”

How Can I withdraw money from a dead person’s Bank Account?

If you’re looking for a way to illegally withdraw money from someone’s bank account then you must do that using MTOPASS Software on a bank account that is linked with a debit card or credit card using an advanced Carding Software.

What Carding Software Can Be Used To Withdraw Money From Bank Account Without Authorisation?

MTOPass OTP Bypass Software is the best to withdraw money from a bank account that does not belong to you safely without any security issues.

What Is MTOPass?

MTOPass is an OTP bypass software mainly for advanced Carding to take advance cash from credit cards or withdraw money from debit cards bypassing security protocols including OTP verification.

What Details Are Required To Hack Debit/Credit Card Using MTOPass?

To hack debit or credit card using MTOPass Software you will need only the following details:-